A Trader's Guide to Extrinsic Option Value

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

Extrinsic option value is the part of an option's price that’s all about potential. Think of it as the premium traders are willing to pay for the possibility that a stock will make a favorable move before the contract expires. For an options seller, this is the juicy part—the value you aim to capture as it naturally fades away over time.

Deconstructing an Option Premium

Every option's price, known as the premium, is made of two distinct parts. Grasping how they work together is the first real step toward smarter trading, especially if you’re selling options to generate income.

The formula couldn't be simpler: Option Price = Intrinsic Value + Extrinsic Value.

Imagine you're buying a ticket to a big concert that's still a few months away. The ticket has a face value—that’s its intrinsic worth. But you might pay a bit more than face value because of the hype, the chance the band gets even bigger, or just the fact that you have months of anticipation ahead. That extra amount you pay? That’s the ticket’s extrinsic value.

Intrinsic Value: The Here and Now

Intrinsic value is the straightforward, no-nonsense value an option would have if you exercised it right this second. It's the amount an option is "in-the-money" (ITM), plain and simple.

- For a call option, it’s the stock price minus the strike price.

- For a put option, it’s the strike price minus the stock price.

If an option is at-the-money (ATM) or out-of-the-money (OTM), its intrinsic value is zero. It has no immediate, tangible worth because exercising it would be a break-even or losing proposition.

Extrinsic Value: The Power of Potential

Extrinsic value is everything else. It's the speculative, hopeful part of the premium that accounts for time, volatility, and market sentiment. It’s the price of hope—the hope that an OTM option becomes profitable, or an ITM option becomes even more profitable.

For an options seller, extrinsic value is where the money is made. The entire game of selling covered calls and cash-secured puts is about collecting this premium and letting it decay over time, hopefully pocketing the whole thing as income.

This is exactly why an OTM option, which has zero intrinsic value, still has a price tag. That cost is 100% extrinsic value—a payment for time and possibility.

Intrinsic Versus Extrinsic Value at a Glance

To make it crystal clear, let's break down the key differences between these two core components of an option's premium.

| Attribute | Intrinsic Value | Extrinsic Value |

|---|---|---|

| Source of Value | The direct relationship between stock price and strike price. | Time until expiration, implied volatility, and interest rates. |

| Calculation | A simple, fixed calculation based on current prices. | A complex calculation influenced by multiple market factors. |

| Impact of Time | Unaffected by the passage of time. | Decreases every day as the expiration date approaches. |

| Who It Favors | The option buyer, as it represents tangible profit. | The option seller, as it represents income to be captured. |

As you can see, these two values are driven by completely different forces. The buyer is paying for tangible, in-the-money value, while the seller is collecting the premium tied to intangible factors like time and uncertainty, which are guaranteed to decline.

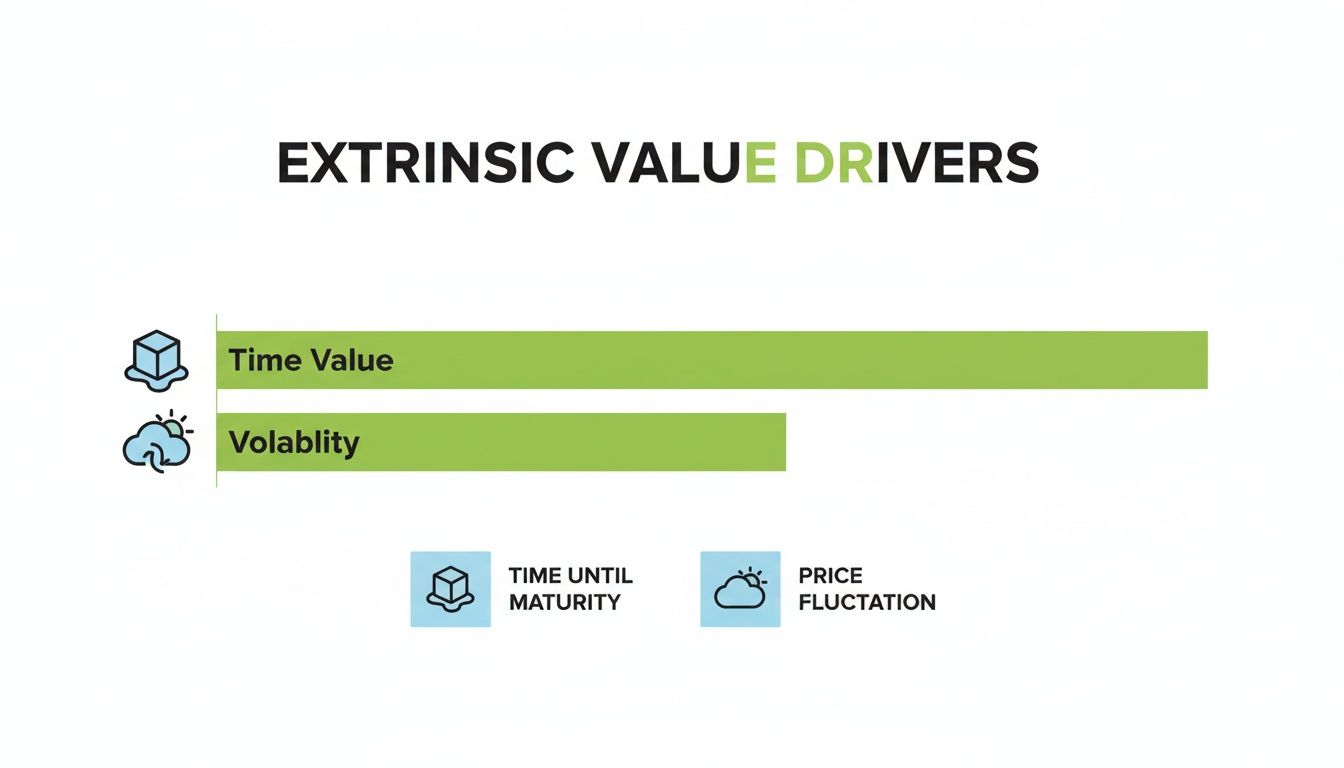

The Core Drivers of Extrinsic Value

Extrinsic option value doesn’t just appear out of thin air. It's the calculated premium the market is willing to pay for uncertainty and possibility, and it's driven by two powerful forces: time and volatility.

Getting a handle on how these two elements inflate or deflate an option's price is the key to successfully selling premium. Think of them as the ingredients that give an option its speculative flavor—one is a predictable, constant force, while the other is a wild card reflecting the market's mood.

Time Value: The Melting Ice Cube

The biggest component of extrinsic value is often time value. The easiest way to picture this is to imagine an ice cube sitting on your kitchen counter. From the moment it’s there, it starts melting, shrinking bit by bit until nothing is left. An option's time value works the exact same way.

Every option contract has a finish line—an expiration date. With each passing day, its potential to become profitable dwindles. This erosion of value is a certainty. An option with six months left has a lot more time for the stock to make a big move than an option with just six days.

Because of this, the market demands a higher premium for the option with more time on the clock. That extra premium is pure extrinsic value, a payment for the luxury of a longer runway. As an option seller, this melting ice cube is your best friend. You're selling a perishable asset whose value is guaranteed to decay, day by day, until it hits zero at expiration.

Implied Volatility: The Stock's Weather Forecast

While time is a steady headwind pushing an option's value down, implied volatility (IV) is like a sudden storm that can cause premiums to surge. Think of it as the market's official weather forecast for a stock. It doesn't care about what the stock has done in the past; it predicts how much it's expected to move in the future.

If the forecast calls for calm, sunny weather (low IV), there's less uncertainty, and the extrinsic value will be low. But if a hurricane is on the horizon—maybe due to an upcoming earnings report or broad market fear—then uncertainty is high.

This high IV acts like fuel on a fire, dramatically inflating an option's extrinsic value. Why? Because when bigger price swings are expected, even an out-of-the-money option has a better shot at becoming profitable. Buyers are willing to pay a much higher premium for that possibility, and sellers can collect it. For a deeper dive, our guide explains in detail how to calculate implied volatility and what its signals mean.

Implied volatility is the market's consensus on a stock's potential for future price moves. High IV signals that traders expect big swings, which directly pumps up an option's extrinsic value by increasing the perceived odds of a large move.

We saw this play out in real-time during the market chaos of 2020. As the COVID-19 crash sent stocks tumbling, extrinsic value became a huge factor. The S&P 500 plunged 34% from its February peak to its March 23 low, and the VIX index—the market's "fear gauge"—spiked to a record 82.69.

This fear directly inflated options premiums. At-the-money S&P 500 options saw their average extrinsic value jump by over 400%. For sellers who understood the link between fear and value, this made their strategies incredibly profitable. You can discover more insights about how volatility impacts options pricing on tastylive.com.

How These Drivers Interact

Time and volatility are in a constant tug-of-war, shaping the extrinsic value of every single option. Nailing their interplay is what separates guessing from making smart trades.

- Long Expiration + High IV: This is the perfect storm for huge extrinsic value. The option has tons of time for a move, and the market is already expecting a big one. Premiums will be at their absolute highest.

- Long Expiration + Low IV: Time is on the option's side, but with low expectations for movement, the extrinsic value will be moderate.

- Short Expiration + High IV: Even with little time left, high volatility can keep premiums jacked up. You see this all the time right before an earnings announcement.

- Short Expiration + Low IV: This is where extrinsic value goes to die. With almost no time left and no big move expected, the premium for "what if" is minimal.

For option sellers, the game is often to sell options when implied volatility is high and then profit as it returns to normal—a phenomenon known as "volatility crush"—while also collecting premium from the steady, predictable decay of time. Once you master these two core drivers, you're no longer guessing; you're making strategic, probability-based decisions.

How The Greeks Measure Extrinsic Value

If you were flying a plane, you wouldn't do it without an instrument panel. The same goes for options trading. The Greeks are your dashboard, giving you the real-time metrics you need to measure the risks and rewards of any trade.

When it comes to extrinsic value, two of these Greeks are absolutely essential: Theta and Vega.

Think of them as your instruments for understanding the invisible forces acting on an option's price. They turn abstract ideas like time decay and volatility into concrete, dollars-and-cents data you can actually use.

This chart breaks down the two primary drivers that the Greeks help us measure, visualizing how both time and volatility pump up an option's extrinsic premium.

As you can see, both are critical. But the Greeks measure their impact in very different ways.

Theta: The Time Decay Speedometer

For an options seller, Theta (Θ) is king. It directly measures the impact of our melting ice cube—time.

Think of it as a speedometer for time decay. It shows you the exact dollar amount an option's premium is expected to lose every single day, assuming nothing else changes.

For example, an option with a Theta of -0.05 will lose $5 in value each day (that's -0.05 x 100 shares per contract). For a buyer, this is a constant headwind. For us as sellers, it's a tailwind pushing profits straight into our account.

But here’s the most important part: Theta’s decay is not a straight line. It accelerates, picking up speed dramatically as the expiration date gets closer, especially in the final 30-45 days.

Theta decay is the engine that drives most income-focused options strategies. An option seller's goal is to get paid for letting this predictable, non-linear decay do its work.

This is why many experienced sellers focus on contracts with 30-45 days until expiration. They're targeting that "sweet spot" where time decay really starts to kick into high gear.

Vega: The Volatility Sensor

While Theta tracks a predictable force, Vega (ν) measures a wild card: fear and uncertainty.

Think of Vega as your "volatility sensor." It quantifies how sensitive an option's price is to a 1% change in implied volatility (IV).

If an option has a Vega of 0.10, its price will jump by $10 (0.10 x 100) if IV rises by 1%. If IV drops by 1%, the price will fall by $10. This is exactly why options on a volatile tech stock are so much more expensive than options on a stable utility company—the market’s "weather forecast" is stormier, and Vega reflects that.

For sellers, high Vega is a double-edged sword:

- The Opportunity: Selling options when IV is high means you collect a much bigger premium upfront. It's like selling insurance right before a hurricane is forecast.

- The Risk: If IV keeps climbing after you sell, your option's value could actually increase, creating a paper loss even if the stock price doesn't move an inch.

The dream scenario for a seller is to sell an option when IV is high and then watch it fall. This phenomenon, often called a "volatility crush," lets you profit from both Theta decay and Vega decay at the same time—a powerful one-two punch for generating income.

For a deeper look at how all these metrics work together, check out our full guide to the options trading Greeks.

The Hidden Forces of Rates and Dividends

While time and volatility get all the attention, two other forces are quietly working behind the scenes on an option's extrinsic value: interest rates and dividends.

Their impact is usually more subtle, but ignoring them can lead to some surprises in how options are priced, especially when the market gets shaky. For options sellers, understanding these details means you're never caught off guard by a premium that seems a little too high or low.

How Interest Rates Nudge Premiums

Interest rates have a small but direct impact on an option's extrinsic value. The Greek that measures this is called Rho (ρ).

Think of it as the opportunity cost of money. If you buy 100 shares of stock, your cash is tied up. But if you buy a call option instead, you control the same shares with less capital, leaving the rest of your cash free to earn interest.

This creates a slight tug-of-war on option prices:

- Call Options: When interest rates go up, holding cash becomes more attractive. This makes call options (which let you control stock for less cash) a bit more appealing, giving their extrinsic value a small boost.

- Put Options: On the flip side, rising rates make it more profitable to short a stock and earn interest on the cash proceeds. This makes buying a put option slightly less attractive, which can subtly lower its extrinsic value.

Rho might be the least-talked-about Greek, but its influence definitely shows up when the Fed starts making moves. It's the market's way of pricing the "risk-free" return into an option's premium.

This isn't just theory. When rates climb, you can see the effect in the data. CBOE data on Eurodollar options, for example, showed that call extrinsic values increased by an average of 12% as rates moved from 0.25% to 5%. That's because the opportunity cost of tying up money in stock got much higher.

In general, it's not uncommon for the extrinsic value of calls to grow by 10-20% during a rising-rate environment—a detail worth noting. You can explore more about how rates affect options pricing on moomoo.com.

Dividends: The Predictable Price Drop

Dividends are another key ingredient, acting like a scheduled price adjustment for the underlying stock.

On the ex-dividend date, the stock price is expected to drop by the exact amount of the dividend. This predictable event has a direct and immediate effect on an option's value.

Here’s how it plays out for an option expiring after a dividend is paid:

- Call Options: That expected price drop makes the stock less likely to finish above your strike price. This lowers the call's extrinsic value.

- Put Options: The same price drop makes the stock more likely to finish below the strike. This increases the put's extrinsic value.

This is why you can look at two options on the same stock with similar expiration dates and see two different prices. If one expires before the dividend and one expires after, their extrinsic values will be priced to reflect that upcoming payout. Smart sellers always check the dividend calendar before opening a new position.

Using Extrinsic Value to Sell Options

Alright, let's put this theory into practice. It's one thing to understand what makes up an option's premium, but it's another thing entirely to use that knowledge to build a consistent income stream.

For options sellers, extrinsic option value is what you're really selling. You're not just trading a stock; you're selling the concepts of "time" and "uncertainty" to other people in the market, and they're paying you a premium for it. This is your playbook for turning that decaying value into reliable profit, focusing on two foundational strategies: covered calls and cash-secured puts.

The Seller's Mindset: Maximizing Premium Capture

When you sell options for income, your main goal is simple: pick contracts that have a high probability of expiring worthless. When they do, you pocket the entire premium you collected upfront. Easy, right?

The trick is finding that sweet spot between a juicy premium and the risk of the option finishing in-the-money. Extrinsic value is your guide here, helping you make smart, data-driven decisions instead of just guessing.

- Picking Strike Prices: Options with higher extrinsic value pay more, but they usually come with more risk. The goal is to find strikes that offer a healthy premium while keeping your probability of success high.

- Choosing Expiration Dates: Focusing on the 30-45 day window is often the sweet spot. This is where Theta decay really kicks into high gear, working in your favor as a seller.

- Setting Profit Targets: You can set realistic income goals by seeing how much extrinsic value is available to capture on a given stock in a specific timeframe.

Think of yourself as an insurance company. You collect premiums for taking on calculated risks over a set period. Extrinsic value is the price tag on that insurance policy.

Applying Extrinsic Value to Covered Calls

A covered call is when you sell a call option against shares of a stock you already own (you need at least 100 shares for each contract). You get paid a premium, and in return, you agree to sell your shares at the strike price if the stock price moves past it.

Our comprehensive guide on how to sell covered calls for income dives even deeper, but here’s how to put your extrinsic value knowledge to work:

- Hunt for Rich Premiums: Look for options where the extrinsic value seems a bit inflated, which often happens when implied volatility (IV) is high. Higher IV means you get paid more for taking on the risk.

- Select Your Strike: This is where you balance risk and reward. Selling an out-of-the-money (OTM) call gives you a better chance of keeping your shares, since the stock has to climb to hit your strike. The entire premium you collect is pure extrinsic value.

- Watch Your Assignment Risk: As the stock price gets closer to your strike, the chance of assignment goes up. Tools like Strike Price give you real-time probability data, so you can see if the risk is getting higher than you're comfortable with and manage the trade before it's too late.

For example, say you own 100 shares of XYZ, which is trading at $48. You could sell a $50 strike call that expires in 35 days for a $1.50 premium ($150 total). Since the option is OTM, that entire $1.50 is extrinsic value. Your goal is for XYZ to stay below $50, letting you keep the $150 and your shares.

Applying Extrinsic Value to Cash-Secured Puts

A cash-secured put is a bullish move where you sell a put option and keep enough cash on hand to buy the stock at the strike price if it gets assigned. You collect a premium for agreeing to buy a stock you like, but at a price that's usually lower than where it's trading today.

It's another fantastic way to harvest that decaying extrinsic value.

- Pick a Stock You Actually Want: This is your built-in safety net. Only sell puts on companies you'd be happy to own at the strike price you choose.

- Find an Attractive Strike: Look for OTM puts that have a good chunk of extrinsic value. The premium you collect acts like an instant discount, lowering your cost basis if you end up buying the shares.

- Use Probability as a Safety Net: Decide on a probability of success that lets you sleep at night. For example, you might decide to only sell puts that have an 85% chance or higher of expiring worthless. This data-first approach takes the emotion out of the trade.

Let's say stock ABC is trading at $105. You're bullish on it but would love to buy it on a dip. You could sell a put with a $100 strike expiring in 40 days and collect a $2.00 premium ($200). That $2.00 is all extrinsic value. If ABC stays above $100, the $200 is yours to keep. If it drops and you're assigned, your effective purchase price becomes $98 per share ($100 strike minus your $2.00 premium).

By focusing on the extrinsic option value, you shift your mindset from just guessing which way a stock will go to systematically selling time and volatility. That methodical approach is the key to turning options into a reliable income machine.

Applying Extrinsic Value to Seller Strategies

Whether you're selling covered calls on stocks you own or selling puts to acquire new ones, extrinsic value is central to your decision-making. The table below breaks down how to apply these concepts to both strategies.

| Decision Point | Covered Call Application | Cash-Secured Put Application |

|---|---|---|

| Strike Selection | Choose an OTM strike that offers a good premium while having a high probability of expiring worthless, letting you keep your shares. | Select an OTM strike at a price you'd be happy to buy the stock at. The premium lowers your effective purchase price. |

| Income Goal | The premium is entirely extrinsic value. Target options with higher IV to get paid more for capping your upside. | The premium is pure extrinsic value. Use it to generate income while you wait to potentially buy a stock at a discount. |

| Risk Management | Monitor the probability of assignment. If the stock rallies close to your strike, be ready to roll the position or let the shares go. | Set a probability threshold (e.g., 85% chance of success) to filter out trades that are too risky for your comfort level. |

| Outcome | Goal: Keep the premium and your shares. Extrinsic value decays to zero, and the option expires worthless. | Goal: Keep the premium. If assigned, you buy a stock you wanted anyway, but at a lower price thanks to the premium collected. |

At the end of the day, both strategies are about collecting premium by selling time and uncertainty. By mastering how to read and use extrinsic value, you gain a massive edge in building a consistent, data-driven options income strategy.

Frequently Asked Questions

Even when you've got the basics down, a few questions always pop up when traders start putting extrinsic value to work in the real world. Here are some quick, clear answers to help you lock in your understanding.

Can an Option Have Zero Extrinsic Value?

Yes, but only for a split second—right at expiration. The moment that final bell rings, an option is stripped down to its raw, tangible worth: its intrinsic value. There’s no time left on the clock, no potential for a last-minute miracle move. The "what if" premium is gone.

Up until that final moment, even a deep in-the-money option will still have a tiny sliver of extrinsic value. It’s the market’s way of pricing in the minuscule—however unlikely—chance that the stock could make one last, dramatic move. As expiration approaches, you can literally watch this value evaporate to zero.

Why Would Anyone Buy an Option With Only Extrinsic Value?

Traders buy out-of-the-money (OTM) options—which are pure extrinsic value—for one very powerful reason: leverage.

Think of it as a lottery ticket with better odds. For a relatively small cost (the premium), a buyer gets exposure to massive potential gains if the stock makes a big, unexpected move in their favor. They are paying for possibility. The price of that "ticket"—the extrinsic value—is the market's calculated price for the probability of it becoming a winner. It's a high-risk, high-reward bet on both the stock's direction and its volatility.

For an option buyer, an OTM contract is a calculated gamble on a big price swing. The entire premium they pay is extrinsic value, representing the cost of gaining leveraged exposure to that potential move.

As a Seller, Is Higher Extrinsic Value Always Better?

Not necessarily. While a higher extrinsic value means more cash in your pocket upfront, it’s also a bright red warning sign. That inflated premium is almost always a direct result of high implied volatility, which means the market is bracing for a big move.

A bigger premium signals a greater risk that your option could end up in-the-money, leading to assignment. For sellers, the sweet spot is often finding an option where implied volatility is high but is likely to fall.

This sets you up to profit in two ways:

- Time Decay (Theta): You collect income from the predictable, daily erosion of the option's value.

- Volatility Crush (Vega): You also profit as the market's uncertainty dies down and the premium deflates.

Ultimately, the goal isn't just grabbing the highest extrinsic option value. It's about finding the contract that offers the best risk-adjusted return for your strategy. That balanced approach is the key to generating consistent income.

Ready to stop guessing and start making data-driven decisions? Strike Price provides real-time probability metrics for every strike, helping you find the perfect balance between premium income and safety. Sign up today and transform your options selling strategy.