Trading Extrinsic Value in Options for Higher Returns

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

When you buy an option, its price, or premium, is made up of two distinct parts. Extrinsic value is the slice of an option's premium that isn’t tied to its real, immediate worth—it’s the "hope" or "potential" that the option will gain value before it expires.

Decoding an Option's Total Price

Think of it like buying a ticket to the Super Bowl months in advance. The ticket has a face value, which guarantees you a seat in the stadium. That’s its intrinsic value—a concrete, real benefit you can claim right now.

But you probably paid a lot more than face value, right? That extra cost is the ticket's extrinsic value. It’s the price of anticipation, speculation, and time. It represents the collective bet that your team might just make it to the big game.

The Anatomy of an Option Premium

Every single option premium can be broken down with this simple formula:

Option Premium = Intrinsic Value + Extrinsic Value

This is the bedrock of options pricing. Intrinsic value is the easy part; it’s just the amount an option is already in-the-money (ITM). If an option is at-the-money (ATM) or out-of-the-money (OTM), its intrinsic value is $0.

You can dig deeper into the core differences between intrinsic vs extrinsic option value in our full guide.

So, what’s extrinsic value? It's everything else. It’s the risk premium that sellers collect from buyers who are paying for the possibility of a big price move down the road.

To make this crystal clear, here’s a quick side-by-side look at the two components of an option's premium.

Intrinsic Value vs Extrinsic Value at a Glance

| Characteristic | Intrinsic Value | Extrinsic Value |

|---|---|---|

| Source of Value | How much the option is in-the-money | Time, volatility, and market sentiment |

| Exists For | Only In-the-Money (ITM) options | All options (ITM, ATM, and OTM) |

| Changes With | Stock Price vs. Strike Price | Time decay and shifts in implied volatility |

| Value at Expiration | The in-the-money amount, or zero | Always decays to zero |

| Seller's Goal | Manage this risk (if any) | Capture this as pure profit |

This table shows why sellers focus so intently on extrinsic value—it's the only part of the premium that's guaranteed to disappear by expiration.

Why Extrinsic Value Is the Whole Game for Sellers

If you're selling covered calls or cash-secured puts, understanding extrinsic value is everything. You aren't just selling a contract; you're selling "time" and "potential" to other traders. For these income strategies, extrinsic value isn't just a part of the price—it's your entire profit engine.

This "potential" is driven by two main forces:

- Time Until Expiration: The more time left, the bigger the window for the stock to make a profitable move. Time is a wasting asset that benefits the seller.

- Implied Volatility (IV): This is the market’s best guess on how much a stock will swing around. More uncertainty means a higher premium.

An option expiring in six months will have way more extrinsic value than one expiring this Friday. Likewise, an option on a volatile meme stock will carry a much richer extrinsic value than one on a sleepy blue-chip company. This is where the opportunity lies.

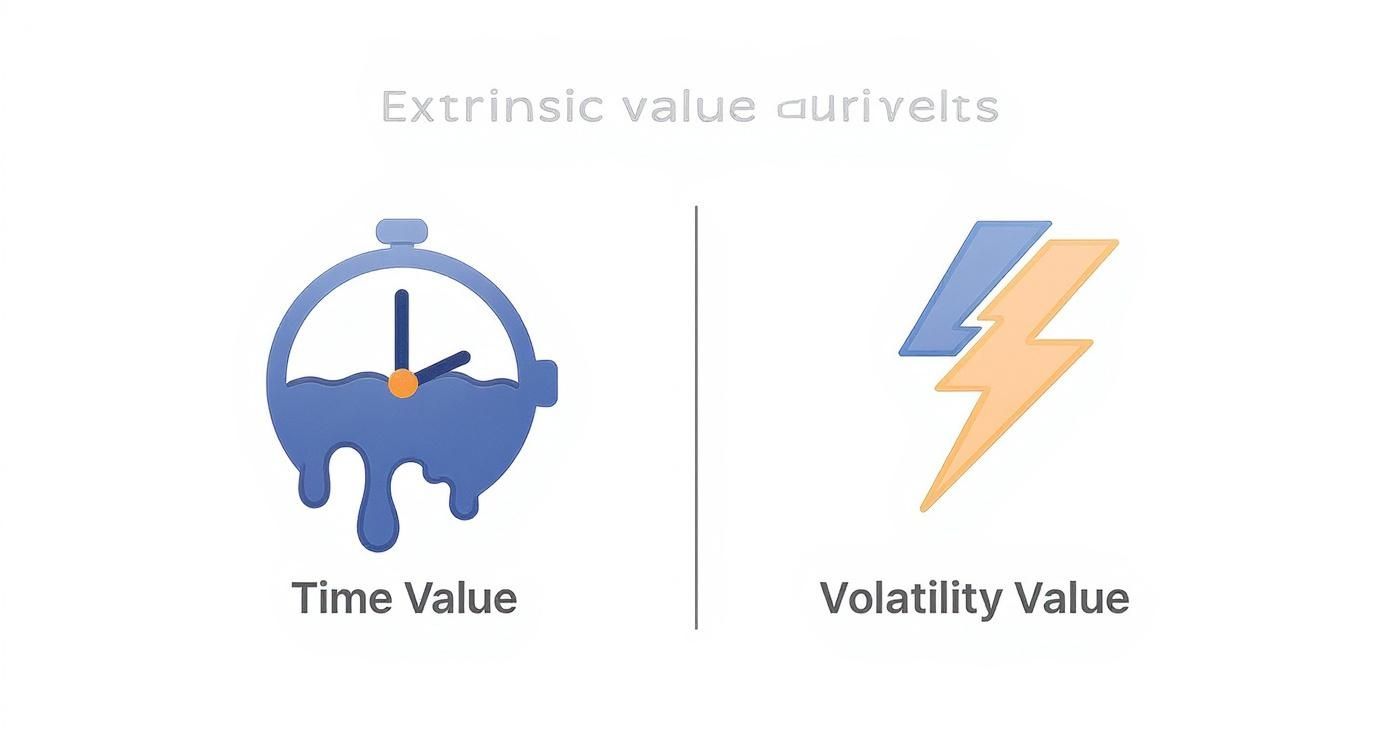

The Two Engines Driving Extrinsic Value

So, where does extrinsic value actually come from? It’s not just a random number. It's the sum of two powerful, distinct forces: time and volatility.

Think of them as the two engines that give an option its speculative juice. One is a steady, predictable countdown. The other is a wild card, reacting to market fear and greed. For anyone selling options for income, these aren't just textbook terms—they're the very assets you're selling.

Time Value: The Melting Ice Cube

The first and most straightforward part of extrinsic value is time. Every option has an expiration date, a finite lifespan. The more time left on the clock, the more opportunity there is for the stock to make a big move in the buyer’s favor.

The best way to think about it is like holding an ice cube.

When you first get it, it’s a solid block. But every second that ticks by, it melts a little, shrinking until nothing is left. An option's time value works exactly the same way. This predictable decay is known as Theta.

An option with six months until it expires has a much bigger "ice cube" of time value than one expiring this Friday. Why? Because that longer runway gives the stock more chances to pop on an earnings report, get swept up in a market rally, or react to unexpected news.

This potential is what buyers pay for. For a buyer, time is a depleting resource. But for a seller, that steady melting is your primary source of profit.

And here’s the kicker: the melting isn't linear. It accelerates. The value an option loses in its final 30 days is often way more than it lost in the months prior, creating a sweet spot for option sellers to capture premium.

Implied Volatility: The Stormy Weather Forecast

If time is a predictable countdown, implied volatility (IV) is the wild, unpredictable weather forecast. It’s the market’s collective guess on how much a stock’s price is going to swing around in the future.

Think of it like buying homeowner's insurance. A policy for a house in a calm, quiet suburb is cheap. But a policy for the exact same house in the middle of a hurricane zone? The premium will be sky-high. The asset is the same, but the perceived future risk is worlds apart.

Implied volatility works just like that.

Low Implied Volatility: This is a forecast for clear skies. The market isn’t expecting much action, so the "insurance premium" baked into the option's price is low.

High Implied Volatility: This is a hurricane warning. The market is bracing for big moves, maybe from an upcoming earnings call, an FDA decision, or just broad market jitters. This fear inflates the extrinsic value, making options a lot more expensive.

This is why two options on different stocks—even with the same strike price and expiration date—can have totally different prices. An option on a sleepy utility stock will have low IV and a tiny extrinsic value. Meanwhile, an option on a biotech stock ahead of clinical trial results could have massive IV and a huge extrinsic value.

For option sellers, high IV is a major opportunity. It means you can sell that "insurance" for a much higher premium. You’re essentially getting paid more to take on the market's perceived risk. The classic play is to sell premium when the forecast is stormy, then let the storm pass—allowing both time and a drop in volatility to erode the option’s price.

How Time Decay Melts Away Your Premiums

Of all the forces pushing and pulling on an option's price, time decay is the only one you can count on. It's a near-certainty. Every single day that ticks by, a little piece of an option's extrinsic value vanishes into thin air, relentlessly dragging its premium down. We measure this steady erosion with the option Greek called Theta.

For those of us selling options, Theta is our best friend. Think of it as earning a little bit of interest just for being patient and letting the clock run. For buyers, though, it’s a constant battle—a ticking clock that’s actively working against their position. This is exactly why a stock can move in the direction a buyer wants, yet their option can still lose money. Time decay is simply chewing through the premium faster than the stock's movement can add value.

And this decay isn't a slow, even drip. It’s more like a snowball rolling downhill. It starts off slow, but it picks up speed and turns into an avalanche in the final weeks before expiration.

The Acceleration of Time Decay

An option with six months left on the clock loses very little value day-to-day. But an option with only 30 days until it expires? Its value melts away at a much, much faster clip. This is the core principle that premium-sellers build their entire income strategy around.

Why the sudden rush? When there’s plenty of time left, a world of possibilities exists for the stock price. But as the expiration date gets closer, that window of opportunity for a big price swing starts to slam shut. All the "hope" and "potential" that was priced into the option dwindles fast, and its extrinsic value goes right along with it.

This is a great way to visualize the two main ingredients of extrinsic value—time and volatility—that sellers are trying to capture.

While volatility can be unpredictable like a lightning strike, time decay is a predictable force, like a melting clock, that consistently erodes an option's premium.

This non-linear decay creates a strategic "sweet spot" for sellers.

- 90+ Days Out: Time decay is painfully slow. You'll collect a premium, sure, but it will erode at a snail's pace.

- 30-45 Days Out: This is where the magic happens. Theta decay speeds up dramatically, letting sellers capture premium at an ideal rate.

- Under 14 Days Out: The decay is incredibly fast, but this period is also loaded with risk (what traders call gamma risk), where even small stock price moves can cause huge, wild swings in your option's value.

For most sellers, the 30-45 day window hits the perfect balance between collecting solid premium and keeping risk at a manageable level. It lets you ride the steepest, most profitable part of the time decay curve without getting caught in the chaos of the final expiration week.

The Real-World Impact of Time on Your Premium

The amount of time left on the clock has a direct, measurable impact on the extrinsic value in options. Looking at data from 2010 to 2020, options with over 90 days to expiration carried premiums that were, on average, 40-60% higher than those with less than 30 days to go.

A study on S&P 500 index options during that time found the average extrinsic value for calls expiring in 90+ days was $4.20 per contract. Compare that to just $1.75 for those expiring in under 30 days.

Let's make this real. Imagine stock XYZ is trading at $50.

- Option A: A $50 call expiring in 90 days might cost $3.00. Since it's at-the-money, that's all extrinsic value. Its Theta might be -0.02, meaning it only loses two cents a day.

- Option B: A $50 call expiring in 30 days might cost $1.50. Its Theta could be -0.04, meaning it's losing value twice as fast as the longer-dated option.

As a seller, you could sell Option B, wait 30 days for its value to decay toward zero, and then do it all over again by selling another 30-day option. This cycle of harvesting rapidly decaying premium is the heart of what we call "selling theta."

To really master this concept, check out our complete guide on how time decay in options works. Once you understand this predictable erosion, you can position yourself to let the calendar do most of the heavy lifting for you.

Using Implied Volatility to Your Advantage

https://www.youtube.com/embed/NEakTsocOEU

While time decay is a steady, predictable force chipping away at an option's value, there’s another, more powerful ingredient in the mix: implied volatility (IV).

Think of implied volatility as the market’s collective gut feeling. It’s not about what a stock has done, but what everyone thinks it might do in the future. It’s the wild card.

This "guess" dramatically inflates the extrinsic value in options. It works a lot like car insurance.

Imagine you're insuring two different cars. A dependable family minivan has a low premium because the odds of it getting into a high-speed chase are pretty slim. But a brand-new, high-performance sports car? That’s going to cost a fortune to insure. The potential for something wild to happen is just so much higher.

Options are no different. A stock with low IV is that predictable minivan—its options have cheap extrinsic value. A stock with high IV is the sports car, commanding rich premiums because the market is bracing for big price swings.

Why Volatility Spikes Inflate Premiums

Implied volatility isn't set in stone. It rises and falls based on market news and trader sentiment, and for option sellers, this is where the real opportunity lies.

Certain events are notorious for cranking IV up to eleven:

- Earnings Reports: The days leading up to an earnings release are filled with uncertainty. Will they crush it or miss badly? That unknown sends IV soaring.

- Major News Events: Think FDA drug approvals for a biotech firm, a big product launch, or major economic data releases. Anything with a make-or-break outcome pumps up volatility.

- Broad Market Fear: When the whole market gets rattled, the CBOE Volatility Index (VIX)—the "fear gauge"—spikes. This lifts IV for almost everything.

For option sellers, these high-IV periods are primetime. You get to sell that "insurance" when fear is maxed out and the premiums are juiciest. To really make the most of this, it helps to understand the broader concept of market volatility and how it affects everything.

Volatility in Action: A Real-World Comparison

Let's put this into practice. Picture two different stocks, both trading at $100.

- Stock A (Utility Co): A stable, slow-moving utility company. Its IV is sitting around 20%.

- Stock B (Tech Co): A fast-growing tech stock with a big earnings report next week. Its IV is jacked up to 70%.

An at-the-money call option expiring in 30 days for Stock A might only fetch a $2.50 premium. But for Stock B, that same option could easily be worth $7.00 or more. That entire difference is pure extrinsic value, fueled by the market’s expectation of a massive move.

Key Takeaway: High implied volatility is a multiplier for extrinsic value. As a seller, you're paid more to take on the market's perceived risk when uncertainty is high.

The data backs this up. Between 2015 and 2022, the average IV for S&P 500 options was 18.5%. But during major market shocks, like the sell-offs in 2018 and 2020, it shot past 35%. In those periods, the extrinsic value of options jumped by 50-80% compared to calmer times.

By learning how to spot these IV spikes, you can time your trades to sell premium when it's most expensive. Our guide on how to calculate implied volatility can give you the tools you need to analyze these opportunities. It’s all about collecting more income for the same amount of risk—a cornerstone of smart options selling.

Practical Strategies for Trading Extrinsic Value

Knowing the theory is one thing, but turning it into a steady stream of income is a completely different ballgame. This is where we stop talking about concepts and start talking about action. The most direct way to profit from the extrinsic value in options is to sell it to other traders—the ones willing to pay you for time and possibility.

This simple shift changes the entire trading dynamic. Instead of just betting on where a stock is headed, you're making a bet that time will simply pass. That's it. Strategies like covered calls and cash-secured puts are the bread and butter here. At their core, you’re just selling a contract loaded with extrinsic value and letting time decay do all the hard work for you.

Selecting the Right Strike Price for Maximum Premium

The strike price you pick is easily the single most important decision you'll make as an options seller. It’s the lever that controls your risk, your potential reward, and exactly how much cash you collect upfront.

Here’s how to think about it:

At-the-Money (ATM) Options: These have a strike price that’s right next to the current stock price. Why does that matter? Because they have the highest amount of extrinsic value. There’s maximum uncertainty about whether they’ll finish in-the-money or worthless, and sellers get paid the most for taking on that uncertainty.

Out-of-the-Money (OTM) Options: These strikes are further away from the stock’s current price. They offer less premium, which might sound bad, but they give you a much bigger cushion if the stock moves against you. You trade a little income for a higher probability of success.

While that juicy ATM premium is tempting, most experienced sellers find a much better risk-reward balance with slightly OTM strikes. You collect a bit less cash, but you give the stock more room to breathe without putting your position in danger.

A great rule of thumb for sellers is to look at strikes with a delta between 0.20 and 0.30. This is often the sweet spot—it gives you a healthy amount of premium while keeping the odds of the option expiring worthless stacked in your favor (usually around 70-80%).

This table breaks down how your strike selection shapes the trade:

| Option Type | Intrinsic Value | Extrinsic Value | Primary Goal |

|---|---|---|---|

| In-the-Money (ITM) | Yes (significant) | Low | Often used for stock acquisition or directional bets |

| At-the-Money (ATM) | Zero or very little | Highest | Maximize premium income with higher risk |

| Out-of-the-Money (OTM) | Zero | Medium to High | Balance premium income with a higher probability of success |

Ultimately, choosing a strike is about defining what you want from the trade: maximum cash now or a better chance of keeping that cash later.

Finding the Expiration Sweet Spot

Just as critical as your strike price is the expiration date. As we covered, time decay isn't a straight line—it's a curve that gets much steeper as the clock ticks down. This creates a strategic window where you can collect premium most efficiently.

If you sell options that are too far out (think 90+ days), your money is tied up for a long time while time decay moves at a snail's pace. On the flip side, selling weekly options (under 7 days) is like playing with fire. You expose yourself to wild price swings—what traders call "gamma risk"—where tiny stock movements can cause huge P&L swings.

For most premium-selling strategies, the ideal timeframe is between 30 and 45 days to expiration (DTE).

This window gives you the best of both worlds:

- Accelerated Theta Decay: You jump into the trade just as the time decay curve really starts to nosedive, letting you profit faster.

- Manageable Gamma Risk: You sidestep the chaos and gut-wrenching volatility that often happens in the last few days before an option expires.

This approach lets you run a consistent system: sell an option with 45 days left, manage it for a few weeks, close it for a profit, and roll right into the next 45-day cycle.

Actionable Rules for Premium Sellers

Let’s put it all together into a simple framework for harvesting extrinsic value.

Prioritize High Implied Volatility: Hunt for stocks where implied volatility is higher than its historical average. This is like selling umbrellas when it’s already raining—you get paid more because demand is high.

Choose a 30-45 DTE Expiration: This puts you right in the sweet spot of the time decay curve, where Theta works hardest for you.

Select a Favorable Strike Price: Aim for those slightly OTM strikes (like a 0.30 delta) to get a good balance between the premium you collect and your probability of keeping it.

Manage Winners Actively: Don't get greedy and hold every trade to expiration. A fantastic rule is to take profits once you've captured 50% of the premium you originally sold the option for. Lock it in and move on.

And remember, when you're executing these trades, especially in volatile markets, understanding and managing slippage is key to making sure you actually get the price you're aiming for.

By following these simple rules, you can transform options selling from a guessing game into a repeatable process for generating income from something we know is certain: the passage of time.

Your Questions on Extrinsic Value, Answered

Once you start digging into options, a few common questions always pop up around extrinsic value. It’s the more abstract side of an option’s price, so let's clear up the most frequent points of confusion. Getting these concepts down cold is what separates guessing from confident trading.

Can an Option Have Only Extrinsic Value?

Yes, and most of them do.

Any option that is at-the-money (ATM) or out-of-the-money (OTM) is made up of 100% extrinsic value. Since these contracts have no real, exercisable worth right now (intrinsic value is zero), their entire market price is a bet on time and potential.

It’s like buying a ticket to a championship game at the beginning of the season. The ticket's value isn't based on a win today; it's based entirely on the possibility of a future win. That possibility is its extrinsic value.

Do In-the-Money Options Have Extrinsic Value?

They sure do. As long as an option has time left before it expires, it will have some extrinsic value, even if it’s deep in-the-money (ITM).

But the dynamic shifts. The deeper an option goes in-the-money, the less extrinsic value it holds. Its price becomes almost entirely dominated by its tangible, intrinsic value. Why? Because there’s much less uncertainty about where it will end up. Traders just aren't willing to pay a big premium for "hope" when the outcome looks more and more like a sure thing.

A deep in-the-money option starts acting a lot like the stock itself. The speculative part—the extrinsic value—dwindles, leaving behind nearly pure, practical worth.

Which Options Have the Most Extrinsic Value?

The peak of extrinsic value is always found in at-the-money (ATM) options.

This is where uncertainty is at its highest. The stock is trading right at the strike price, giving the option a roughly 50/50 shot of expiring worthless or finishing in-the-money. This maximum uncertainty commands the highest premium for time and volatility.

- Out-of-the-Money (OTM): Less extrinsic value because the odds of them becoming profitable are lower.

- In-the-Money (ITM): Also less extrinsic value because their outcome is getting more predictable.

For sellers, ATM strikes dangle the richest premiums. Just remember, that reward comes with the highest risk of the stock price moving against you.

Why Is This So Important for Option Sellers?

For anyone selling covered calls or secured puts, extrinsic value isn't just part of the equation—it's the whole prize. It is the only part of the premium you can capture as pure profit.

When you sell an option, you’re collecting an upfront payment that’s packed with this time and volatility value.

From there, your goal is simple: let that value decay. Every day that passes, time decay (Theta) chips away at the option's extrinsic value. If all goes to plan, the option expires worthless, and every penny of the premium you collected is yours to keep. This predictable erosion is how option sellers turn the passage of time into a consistent income stream.

Ready to stop guessing and start selling options with data-driven confidence? Strike Price provides real-time probability metrics for every strike, helping you balance safety and premium income. Get smart alerts, track your portfolio, and find high-reward opportunities tailored to your risk tolerance. Transform your options selling from a gamble into a strategic, income-generating process. Join thousands of successful sellers on Strike Price today!