Margin Call Calculation: A Practical Guide to Protecting Your Portfolio

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

Getting a margin call is one of the most stressful things a trader can experience. But if you understand how the margin call calculation works, you're already halfway to preventing one.

Put simply, a margin call is your broker demanding you add more cash or securities to your account. Why? Because the value of your collateral—the stocks and cash you're using to back your loan—has dropped too low, and your account equity needs to be brought back up to a required minimum.

What a Margin Call Really Means for Your Account

Think of a margin loan like a mortgage for your portfolio. You put down some of your own money (initial margin) and borrow the rest from your broker to buy securities. But unlike a house, the value of your collateral is constantly changing with the market.

If the value of your stocks drops hard, your "down payment," or the equity in your account, shrinks right along with it.

When that equity falls below a certain percentage, known as the maintenance margin, it sets off an alarm at your brokerage. That's the margin call. It’s not a friendly suggestion; it's a formal demand to fix your account's health, and you have to act fast.

Initial vs. Maintenance Margin

To really get how this works, you need to know the difference between two key terms:

- Initial Margin: This is the slice of the purchase price you have to cover with your own money when you first buy a stock on margin. Regulation T sets the floor at 50%, but brokers often ask for more, especially for volatile stocks. It's your skin in the game.

- Maintenance Margin: This is the absolute minimum amount of equity you must keep in your account. FINRA requires at least 25%, but most brokers set their "house requirement" higher—often 30% to 40%—to give themselves a safety buffer. Your entire margin call calculation hinges on this number.

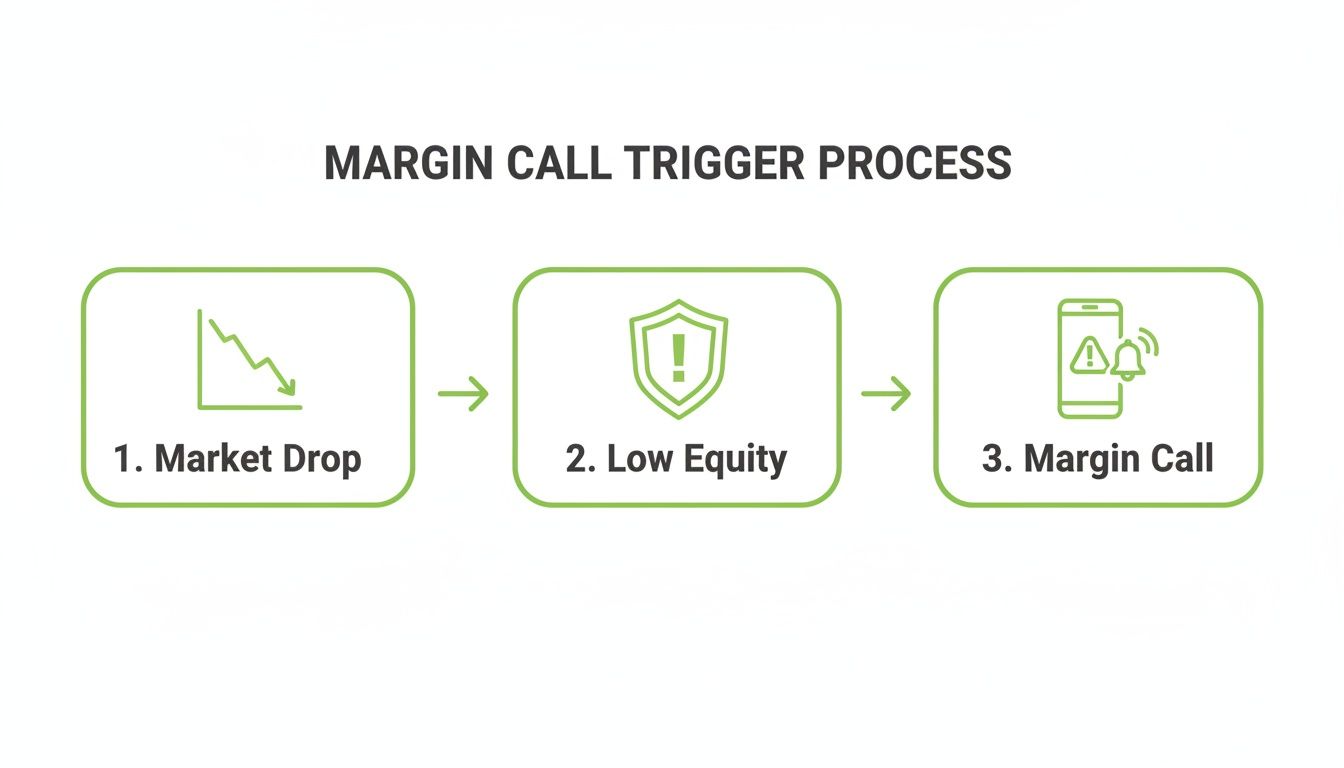

The most common trigger is a stock taking a nosedive. That sharp drop eats away at your account equity, pushing it dangerously close to that maintenance margin threshold. The second your equity percentage dips below that line, the call is issued.

The real problem isn't just that a stock went down. It's that the ratio of your personal equity to the market value of your securities has breached the limit you agreed to. The broker's only concern is protecting the loan they gave you.

Key Margin Terms at a Glance

Getting a handle on margin trading means knowing the lingo. These are the core terms you'll see again and again, and understanding them is non-negotiable if you want to stay out of trouble.

| Term | What It Means for You | Typical Requirement |

|---|---|---|

| Initial Margin | The percentage of the purchase you must fund yourself when you first open a position. | 50% (per Regulation T) |

| Maintenance Margin | The minimum equity percentage you must always maintain in your account. | 25% (FINRA minimum), but often 30%-40% by brokers. |

| Account Equity | Your ownership stake in the account. Calculated as: Market Value of Securities - Margin Loan. | Varies with market fluctuations. |

| Margin Loan | The amount of money you've borrowed from your broker to purchase securities. | The amount you borrowed. |

This table is your quick cheat sheet. If you ever feel lost in the numbers, come back to these definitions—they’re the foundation of every margin calculation.

Widespread margin use can even create risks for the entire market. For instance, margin debt at U.S. broker-dealers peaked at around $936 billion in October 2021. But as the market turned sour, it plunged by roughly 27% by mid-2022, forcing traders to sell assets to cover their calls. You can see this for yourself in FINRA's public data about margin accounts. This shows how a wave of margin calls can pour fuel on the fire during a downturn.

The whole system is built on a strict regulatory framework, which you can explore further in these SEC compliance guidelines. If you can't meet the margin call by adding cash or selling positions, your broker has the right to start liquidating your holdings—without your permission—to pay back the loan. This forced selling can lock in your losses at the worst possible moment, which is why preventing a call in the first place is so critical.

The Core Formulas for Calculating Your Margin Status

To really get a handle on your margin risk, you have to get comfortable with the math. The good news is that the core margin call calculation isn't rocket science; it's just a few key formulas. Mastering them is the difference between reacting to a margin call and preventing one from ever happening.

These calculations live and die by real-time data. The foundation of any solid margin calculation is accurate data acquisition, making sure every number you plug in is reliable and current. Without it, you're just guessing at your risk.

This process shows how a market drop can quickly trigger a margin call. The key takeaway? The call isn't just about the stock price; it's about your account equity getting dangerously low.

Calculating Your Account Equity

First up, let's nail down your account equity. This is the most important number in your margin account because it represents your actual stake in the game—what’s left after you pay back the house.

The formula is straightforward:

Account Equity = Current Market Value of Securities – Debit Balance (Loan Amount)

Let's say you bought 100 shares of XYZ stock at $150 a share, for a total value of $15,000. You put down $7,500 of your own money and borrowed the other $7,500 from your broker. Your initial equity is $7,500.

Now, imagine XYZ stock drops to $120 per share. The total value of your position sinks to $12,000. Your loan is still $7,500, but your equity has shrunk to just $4,500 ($12,000 - $7,500). That drop is what puts your margin status at risk. This core calculation is also a key part of the broader valuation of options and other securities, where the underlying asset's value is everything.

Determining Your Maintenance Requirement

Next, you need to know the absolute minimum equity your broker requires you to keep in the account. This is the maintenance margin requirement, and it's a hard floor.

Here’s how you find that dollar amount:

Maintenance Margin Requirement ($) = Current Market Value x Broker’s Maintenance Margin %

Using our example, let's assume your broker has a 30% maintenance margin. With the stock now at $120 per share (a $12,000 market value), your required equity is $3,600 ($12,000 x 0.30).

Finding Your Excess Margin

Okay, time to put it all together. Your excess margin is the buffer between your current equity and the minimum your broker demands. Think of it as your financial cushion.

Excess Margin = Current Account Equity – Maintenance Margin Requirement

In our scenario:

- Your current equity is $4,500.

- Your maintenance requirement is $3,600.

This means your excess margin is $900 ($4,500 - $3,600). You’re still in the clear, but that cushion is getting pretty thin. The second this number turns negative, the phone will ring.

How to Calculate Your Trigger Price

This is where the math gets really powerful. Instead of just tracking your cushion, you can calculate the exact stock price that would trigger a margin call. This flips your risk management from reactive to proactive.

The formula is a little more involved, but it's worth its weight in gold:

Trigger Price = Debit Balance / (Number of Shares x (1 – Maintenance Margin %))

Let’s run the numbers for our example:

- Debit Balance: $7,500

- Number of Shares: 100

- Maintenance Margin %: 0.30 (or 30%)

Trigger Price = $7,500 / (100 x (1 – 0.30))

Trigger Price = $7,500 / (100 x 0.70)

Trigger Price = $7,500 / 70

Trigger Price = $107.14

This tells you that if XYZ stock drops to $107.14 per share, you'll breach the maintenance margin, and your broker will issue a margin call. Knowing this exact price lets you set alerts or place stop-loss orders well before disaster strikes, putting you back in control of your risk.

How Options Strategies Change the Margin Math

Selling options adds a completely different layer to the standard margin call calculation. Buying stock on margin is one thing, but strategies like covered calls and cash-secured puts come with their own risk profiles that can mess with your account equity in unexpected ways. If you're looking to generate income from options, you have to get this part right.

When you sell an option, that premium hits your account as cash almost instantly. It feels like a quick win, but it also creates an obligation—a promise your broker needs to know you can keep. That obligation is what rewrites the margin math.

Covered Calls and Their Margin Impact

A covered call means you’re selling a call option against stock you already own, typically 100 shares per contract. Since you own the shares, the position is "covered." It’s often seen as a conservative strategy, but it definitely has consequences for your margin account.

The premium you collect from selling the call boosts your cash balance, which bumps up your equity. This can actually give you a little extra margin cushion right at the start. The game changes, though, when the stock price starts moving.

- If the stock price drops: The value of your 100 shares falls, which directly eats into your account equity. That premium you collected helps soften the blow, but a sharp drop can still crater your equity and trigger a margin call, especially if you have other leveraged trades open.

- If the stock price rises: Your shares are worth more, which is great for your equity. But as the stock price screams past your strike price, that short call option starts looking like a bigger and bigger liability. Even though you're covered, some brokers will tighten your maintenance requirement to reflect the growing chance of assignment.

A huge mistake traders make is thinking a covered call is "risk-free" from a margin perspective. You won't face unlimited losses, but a steep dive in the underlying stock can absolutely push you toward a margin call by destroying your account equity.

Cash-Secured Puts and Your Equity

With a cash-secured put, you sell a put option and set aside enough cash to buy the stock if you get assigned. Sell one put with a $50 strike price, and you need to have $5,000 cash parked and ready.

This "secured" cash is the key here. Most brokers will reduce your buying power by the amount needed to secure the put, but that cash is still part of your total account equity. The important thing is that it’s not a debit like a margin loan.

Let's walk through it. Say you have a $20,000 account, all cash. You sell one cash-secured put on stock ABC with a $90 strike, which means you have to secure $9,000.

Your account equity is still $20,000. However, your buying power for any new marginable trades has just dropped to $11,000. That secured cash is earmarked and can’t be used for anything else. If the stock tanks and you get assigned, that $9,000 in cash is swapped for 100 shares of ABC, which will then carry its own maintenance requirement.

How Volatility and Rule Changes Can Surprise You

It's not just price that matters. The whole world of derivatives margining is getting more risk-aware. In recent years, exchanges and clearinghouses have been updating their models, which can seriously ramp up the collateral needed to hold options, especially when the market gets wild.

For instance, some exchanges moved to SPAN2 margining, a system that can hike collateral needs by double-digit percentages when things get choppy. You can dig into how these methodologies are changing by checking out CME Group's historical margin data.

What this means for you is that your broker might dynamically raise your maintenance requirements in response to market volatility—creating a margin call even if your positions haven't moved against you. For traders running more complex strategies, like those we cover in our guide on what an options spread is, these sudden changes can be a big deal. That's where tools like Strike Price come in, helping you model these risks so you can see your true exposure before that dreaded call from your broker arrives.

Navigating Hidden Risks and Edge Cases

A nosedive in your stock's price is the classic margin call trigger, but it's far from the only one. Any seasoned trader can tell you the real trouble often lurks in the edge cases—the sneaky risks that can spark a surprise demand for cash even when you think your positions are solid.

These less-obvious events are what separate a prepared trader from one who gets caught off guard. They can flip your account's leverage ratio on its head without warning, leading to forced liquidations at the absolute worst times.

The Surprise of an Early Assignment

Selling options like covered calls can feel like a relatively safe way to generate income, right up until you're hit with an early assignment. This happens when the option buyer decides to exercise their right to your shares before the expiration date. It might be rare for out-of-the-money options, but it happens. And when it does, it instantly rearranges your account's financial structure.

Picture this: you've sold a covered call against 100 shares of a stock. One morning, you wake up to an assignment notice. Your 100 shares are gone, swapped for cash. If those shares were a key piece of your account's collateral, their sudden disappearance could send your equity percentage plummeting below the maintenance requirement.

Boom. Instant margin call.

This is especially dangerous if that stock was your main non-leveraged asset—the bedrock supporting your other margin positions. Without it, your account's overall leverage can skyrocket overnight.

Dividends and the Assignment Trap

Dividends are another classic trigger for early assignment, particularly with short call options. Think about it from the buyer's perspective. If they want to capture an upcoming dividend, they might exercise their in-the-money call just before the ex-dividend date.

Here's how the trap springs:

- The call buyer exercises their option, forcing you to sell them your shares.

- They get the stock just in time to be the owner of record and pocket the dividend.

- You're left without your shares, which messes with your equity calculation. Or worse, if it was a naked call, you're now short the stock—a position with its own margin requirements.

If you're holding a short call that's in-the-money as an ex-dividend date approaches, the odds of assignment jump dramatically. It's a textbook options "gotcha" that can lead directly to margin trouble.

Pro Tip: Always track ex-dividend dates for any stock you're short calls on. If your call is in-the-money, seriously consider closing or rolling the position before that date. It can save you from a surprise assignment and the margin headache that's sure to follow.

When Volatility Spikes House Requirements

Sometimes, a margin call isn't about you or your specific trades at all. It's about the market's mood. When volatility goes through the roof, brokers get nervous. To shield themselves from risk, they'll often raise their "house" maintenance margin requirements on certain stocks or even across the board.

This means the equity floor you need to maintain just got higher. A position that was perfectly fine with a 30% maintenance requirement could suddenly be in the red if your broker bumps their house rule to 40%. You did nothing wrong, your stock might not have even budged, but you'll still get that dreaded call.

These systemic risks are powerful and easy to overlook. We've seen how forced liquidations from margin calls can create a domino effect during market stress, like with the collapses of Archegos or Long-Term Capital Management. This is precisely why regulators like FINRA keep a close eye on margin debt, which has peaked at over $1 trillion. That's a massive amount of capital sensitive to these sudden shifts. You can find more analysis on the role of margin calls in market downturns on equitiesfirst.com.

By getting a handle on these hidden risks, you can build a portfolio that's resilient enough to handle more than just simple price drops.

Proactive Strategies to Prevent Margin Calls

Knowing the math behind a margin call calculation is one thing, but using that knowledge to stay ahead of the game is where the real power lies. The best way to handle a margin call is to make sure it never happens. This means shifting from reactive panic to proactive risk management—building a solid defense to protect your capital.

This isn't just about avoiding a stressful phone call from your broker. It's about preserving your portfolio’s health and your freedom to trade on your own terms. A forced liquidation can lock in losses at the worst possible time, completely derailing your long-term goals.

Setting Your Personal Risk Thresholds

Your broker’s maintenance margin is their safety net, not yours. They set their limit—often around 30-40%—to protect the money they loaned you. Your personal threshold should be far more conservative, acting as an early warning system long before their alarms even think about going off.

Many seasoned traders maintain a personal "cushion" of excess margin, refusing to let their account equity drop below 50% or even 60% of their portfolio's market value. This buffer buys them time to adjust positions, add funds without pressure, or simply wait for a temporary market dip to recover.

Your broker's margin limit is a cliff edge. Your personal risk threshold should be a fence built a mile away from it. Don't trade near their limit; trade comfortably within your own.

This buffer is especially critical if you're selling options. A sudden spike in volatility or an unexpected assignment can change your account's leverage profile in an instant. A healthy cash reserve gives you the flexibility to navigate these events without being backed into a corner.

Using Stop-Loss Orders Strategically

A stop-loss order is a simple but incredibly effective tool for capping your downside before it triggers a margin event. By setting an automatic sell order at a price you choose, you define the maximum loss you’re willing to take on any single position.

This becomes especially powerful when you know your "trigger price"—the exact stock price that would push you into a margin call.

- Calculate Your Trigger Price: Use the formulas we've discussed to find the price that would breach your maintenance margin.

- Set the Stop-Loss Above It: Place your stop-loss order at a price comfortably above that trigger price. For example, if your trigger is $107.14, you might set a stop-loss at $112.

- Prevent the Cascade: This simple step ensures the position is closed out before your equity takes a critical hit, preventing the margin call entirely.

Suddenly, the margin call calculation transforms from a post-mortem analysis into a proactive risk management tool. It automates your discipline and takes the emotion out of cutting a losing trade.

The Power of Real-Time Monitoring and Alerts

Manual calculations are great for understanding the mechanics, but they’re just a snapshot in time. The market moves fast, and your risk monitoring needs to keep up. This is where modern tools give you a serious edge, acting as a constant guardian for your account.

Platforms like Strike Price monitor your options positions for subtle shifts in risk that a once-a-day calculation would completely miss. One of the most important metrics to watch is assignment probability. A sudden jump here can be the first sign of trouble that could lead to a margin issue down the road.

Imagine you get an alert that the assignment risk on one of your covered calls has leaped from 5% to 40% because of a news event. That alert is a game-changer. It gives you a critical head start to react thoughtfully instead of in a panic.

You now have time to decide whether to close the position or, if you're more experienced, manage the risk by rolling over options to a later date or a different strike. This kind of adjustment can often neutralize the immediate threat long before it ever affects your margin balance. By bridging the gap between static math and dynamic alerts, you can manage risk intelligently and stay firmly in control.

To tie it all together, here's a practical checklist to help you build a stronger defense against margin calls.

Your Margin Call Prevention Checklist

Running through these strategies regularly can make the difference between trading with confidence and trading on the edge of a forced liquidation.

| Strategy | How It Helps Protect You | Implementation Tip |

|---|---|---|

| Set Personal Thresholds | Creates a buffer zone far above your broker's maintenance margin, giving you time to react to market downturns without pressure. | Decide on a minimum excess margin you're comfortable with (e.g., 50%) and treat it as your "zero" line. |

| Use Stop-Loss Orders | Automates your risk management by closing a position at a predetermined price before it can trigger a margin call. | Calculate the margin call trigger price for your largest positions and set your stop-loss orders comfortably above those levels. |

| Monitor Excess Margin | Keeps you constantly aware of your available cushion. A shrinking excess margin is your earliest warning sign of increasing risk. | Check your excess margin daily. If it drops by more than 10% in a day, review your positions immediately. |

| Reduce Concentration | Prevents a single stock's sharp decline from wiping out a disproportionate amount of your account equity and triggering a call. | No single stock position should make up more than 10-15% of your total portfolio value. |

| Utilize Real-Time Alerts | Leverages technology to notify you of changing risk factors (like assignment probability) instantly, allowing for proactive adjustments. | Use an app like Strike Price to get push notifications when the risk on your options positions changes. |

| Keep a Cash Reserve | Provides the liquidity needed to either add funds to your account to meet a call or to navigate an options assignment without a forced sale. | Aim to keep 5-10% of your portfolio value in cash or cash equivalents that are not subject to margin. |

Think of this checklist not as a set of rigid rules, but as a framework for building disciplined trading habits. The more of these strategies you weave into your routine, the more resilient your portfolio will become.

Common Questions About Margin Calls

Even when you've got the math down, real-world margin trading can throw you some curveballs. Let's walk through some of the most common questions that pop up, so you can handle these situations with a clear head.

Getting these details right is non-negotiable. Being unprepared is a surefire way to get your account wiped out.

What Happens If I Cannot Meet a Margin Call?

If you can't deposit the cash or marginable securities your broker demands, things get ugly, fast. Your broker has the legal right to start liquidating your positions immediately, and they don't need your permission.

Worse yet, they decide what to sell to cover the shortfall, not you.

This forced selling almost always happens at the worst possible moment—usually in a plunging market—locking in your losses at rock-bottom prices. On top of that, it can trigger unexpected capital gains or losses, leaving you with a messy tax situation you didn't plan for. It's a scenario every trader needs to avoid at all costs.

How Quickly Do I Have to Meet a Margin Call?

The timeline is set by your broker, and it can be shockingly short. You might hear about a "T+2" standard (two business days) or even up to five days, but don't count on it. That's not a guarantee.

In a volatile, fast-moving market, brokers can demand you meet the call on the spot—sometimes within hours. They have zero obligation to give you an extension. Always read your margin agreement, but trade with the assumption that you might need to act instantly.

Never assume you have a few days to get your house in order. Your broker's #1 priority is their own risk. In a turbulent market, they can and will act swiftly to protect themselves.

Can I Use My Options to Satisfy a Margin Call?

Generally, no. You can't use existing long options—calls or puts you own—to directly cover a margin call. Brokers don't consider them marginable securities because their value can evaporate quickly, making them terrible collateral.

However, what you can do is close out a profitable options position to generate the cash needed. For example, selling a long call that's deep in the money would immediately dump cash into your account. The key is that you have to convert the option to cash; you can't just hand over the contract itself.

How Does a Risk Monitoring Tool Help Prevent Margin Calls?

Modern risk tools are much more than just simple price alerts; they're an early-warning system. For options sellers, a tool that tracks assignment probability in real-time is an absolute game-changer.

Let's say you see a sudden spike in the assignment probability on a covered call you sold. That's your first red flag. It could signal that the underlying stock is getting volatile or that an ex-dividend date is coming up—both classic triggers for assignment.

Getting assigned on a covered call means your shares are sold off. This can radically change your account's equity and leverage, potentially pushing you straight into a margin call. By alerting you to this rising risk before it happens, a good tool gives you the time you need to manage the position. You can roll the option or just close it out long before it ever threatens your margin balance.

Managing options risk shouldn't be a guessing game. Strike Price provides real-time assignment probability alerts and data-driven insights to help you protect your portfolio. Stop reacting to market events and start proactively managing your positions. See how Strike Price can safeguard your account and enhance your income strategies.