A Practical Guide to the Sell Put Strategy

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

The sell put strategy is a smart way to get paid for simply agreeing to buy a stock you like, but at a price that's lower than what it's trading for today. Think of it as setting your own discount price on a company you want to own anyway. It’s a fantastic method for either generating a steady stream of income or strategically buying into great companies on your own terms.

How Selling a Put Actually Works

Imagine you're offering "stock insurance" to another investor. For taking on the risk that a stock might drop, you get paid an upfront fee, known as a premium. This premium is yours to keep, no matter what happens next.

You're essentially telling the market, "I'm willing to buy 100 shares of this company if the price falls to X." This simple agreement can lead to one of two very favorable outcomes for you, the seller.

The Two Favorable Outcomes

The real beauty of this strategy is its win-win potential. As long as you've picked a stock you genuinely wouldn't mind owning, you can come out ahead whether the stock goes up, down, or sideways.

You Generate Income: If the stock's price stays above your agreed-upon purchase price (the strike price) until the contract expires, the option becomes worthless. The other investor won't use their "insurance," you don't have to buy anything, and you simply pocket 100% of the premium as pure profit.

You Buy Stock at a Discount: If the stock's price does fall below your strike price by the expiration date, you'll be required to buy the shares at that price. But here's the kicker: you're buying a company you already wanted at the exact lower price you chose. Plus, the premium you were paid at the start effectively lowers your purchase price even further.

Understanding the Core Components

Every put-selling trade has a few key parts you'll need to get familiar with. These aren't just jargon; they are the dials you turn to fine-tune your risk and potential reward. For a deeper dive into these mechanics, you can explore our full guide on what is selling a put.

The Golden Rule: The goal is to be completely happy with either outcome. You either walk away with extra cash in your pocket, or you become the owner of a great stock at a fantastic price.

To give you a clearer picture, let's put these components into a simple table.

Sell Put Strategy at a Glance

This table breaks down the key elements of a typical cash-secured put trade using a hypothetical stock.

| Component | Description | Example (Stock XYZ at $50) |

|---|---|---|

| Action | You sell a put option contract. | You sell one XYZ $45 put option. |

| Obligation | You agree to buy 100 shares if the price drops below the strike price. | You agree to buy 100 shares of XYZ at $45 per share. |

| Premium | The upfront cash you receive for taking on this obligation. | You receive $2.00 per share ($200 total) immediately. |

| Best Outcome (Income) | Stock stays above the strike price. The option expires. | XYZ closes above $45. You keep the $200 and the trade is done. |

| Other Outcome (Buy Stock) | Stock falls below the strike price. You buy the shares. | XYZ drops to $43. You buy 100 shares at $45, but your cost is only $43 ($45 - $2 premium). |

As you can see, you either generate income or acquire the stock you wanted at a net cost below your target price. This approach, known as a cash-secured put, is a conservative way to generate returns from the market.

Why Investors Choose This Income Strategy

The put-selling strategy isn't just some abstract theory you read about in a textbook; it’s a hands-on tool that thousands of real-world investors use to hit very specific financial goals. Its appeal comes down to three main benefits that work together to deliver consistent returns, smarter stock purchases, and a bit of built-in risk management.

When you get the hang of it, selling puts can actually turn market volatility from something to fear into something you can work with. At its heart, you're getting paid for your willingness to buy a stock you like, but only at a price you've already decided is a good deal.

Earning a Consistent Income Stream

The most straightforward benefit is the cash—the premium—you collect the moment you sell the put. Think of it as being paid to make a promise: you promise to buy 100 shares of a stock if it drops to a certain price by a certain date.

That premium hits your account right away, and it's yours to keep, no matter what happens next. This creates a cash flow that can supplement your other income, get reinvested, or just build up over time. It’s a lot like earning a dividend on a stock you don't even own yet. For anyone focused on building wealth, this regular income is a huge advantage. It's one of several proven strategies for positive cash flow that investors use to keep money coming in.

This strategy allows you to get paid while you wait. Either the stock never reaches your price and you keep the cash, or it does, and you acquire a company you wanted at a discount.

This is what draws so many people in. You turn your patience into a paying gig.

Acquiring Quality Stocks at a Discount

There’s a common myth that getting the stock "assigned" to you means the trade failed. For smart investors, that's often exactly what they were hoping for. Selling a put is a fantastic way to buy shares in a company you already believe in for less than what everyone else is paying on the open market.

You get to set your price. Let's say a stock is trading at $105, but you think it's a steal at $100. You can sell a put with a $100 strike price. If the stock dips and you get assigned, you've achieved your goal—buying a great company at the exact price you wanted. This disciplined method keeps you from emotionally chasing high-flying stocks and lets you enter the market on your own terms.

Lowering Your Cost Basis

The premium you collect isn't just income; it’s also a financial cushion. That cash immediately lowers your "effective" cost if you do end up buying the shares. This is one of the most powerful risk-management aspects of selling puts.

Here’s a simple breakdown of how it works:

- Your Goal: You want to own shares of Company ABC, currently trading at $52. You'd feel much better buying it at $50.

- Your Action: You sell one put contract with a $50 strike price. For this, you collect a premium of $1.50 per share (that's $150 in your pocket, since one contract equals 100 shares).

- The Outcome: The stock price drops to $49. Your put is exercised, and you're assigned the shares at your strike price of $50.

So, you paid $5,000 for 100 shares. But don't forget the $150 premium you already pocketed. Your actual, all-in cost for the stock is only $4,850, which comes out to $48.50 per share.

The premium gave you an instant discount, creating a buffer against any further price drops and giving your new investment a head start. This is how the strategy helps you manage risk right from the get-go.

Navigating the Real Risks and Rewards

Every single investment strategy has a trade-off. It’s a classic seesaw of risk versus reward, and before you jump in, you need to understand both sides of the equation. Selling puts is no different—it offers a clear path to generating income, but it comes with specific risks that demand your respect.

On the bright side, the reward is immediate and tangible: the premium. The moment you sell the put, that cash hits your account, giving you an instant return on your capital. When done consistently, collecting these premiums can become a powerful income stream that adds a steady boost to your portfolio's performance.

But there’s always a flip side. The primary risk is the obligation to buy the stock if it drops in price. If the market takes a nosedive and the stock price falls below your strike price, you're on the hook to buy 100 shares per contract at that higher price. This can result in an immediate paper loss, so you need to be prepared for that possibility.

The Defined Reward Potential

The beauty of selling a put is how straightforward the reward is. Your maximum profit is capped at the premium you collect when you open the trade. That’s it. This defined, predictable profit is what draws in so many income-focused investors who prefer consistent returns over chasing speculative home runs.

Let's look at a quick example. Say you sell a put with a $45 strike price on a stock and collect a $1.50 per share premium. Your maximum profit is locked in at $150 (100 shares x $1.50). This works out to a 3.33% return on the cash you had to set aside to secure the trade ($1.50 premium / $45 strike price)—a pretty solid yield for a short-term commitment.

Historically, this strategy has held up well, offering attractive risk-adjusted returns compared to just buying and holding stock. The Chicago Board Options Exchange even tracks indices like the CBOE S&P 500 PutWrite Index (PUT). While these strategies sometimes trail the S&P 500 in roaring bull markets, they often perform better during downturns because that premium income acts as a buffer. You can dig deeper into the data on how selling put options has performed historically.

The sell put strategy trades unlimited upside potential for a high probability of a limited, but consistent, profit. It's a game of singles and doubles, not home runs.

Confronting the Core Risks

While the reward is defined and easy to understand, the risks are where you need to pay close attention. Acknowledging these potential downsides isn't about scaring you off; it's the first step toward building a resilient strategy that can handle whatever the market throws at it.

1. The Assignment Risk

This is the big one. If the stock’s price plummets below your strike, your obligation to buy the shares gets triggered. Imagine you sell a $100 put and the stock craters to $80 by expiration. You are now required to buy those shares for $100 each, locking in an instant $20 per share unrealized loss. The premium you collected helps lower your net cost, but a severe drop can still sting.

2. The Opportunity Cost

The other major risk is what you're giving up. When you sell a put, you cap your profit at the premium. Let’s say the stock you sold that $100 put on suddenly shoots up to $150. Your profit is still just the small premium you collected at the start. You miss out on that entire $50 run-up. That's the opportunity cost of choosing predictable income over explosive growth potential.

A Balanced View of the Trade-Off

Ultimately, deciding whether to sell puts comes down to your personal financial goals and how much risk you’re comfortable with. It's a fantastic tool for generating a steady income and a clever way to buy stocks you already like at a discount. It is not, however, a get-rich-quick scheme.

This strategy really shines in flat, slightly rising, or even slightly falling markets, where the premiums you collect more than makeup for minor stock price fluctuations. It requires patience, discipline, and a genuine belief in the long-term value of the companies you choose. By understanding that you're trading away the chance for huge gains in exchange for a steady stream of income, you can decide if this powerful strategy is the right fit for your investment philosophy.

How to Place Your First Cash-Secured Put Trade

Reading about a strategy is one thing, but putting it into practice is where the real learning—and earning—begins. Let's walk through exactly how to execute your first cash-secured put, from picking the right company to placing the order in your brokerage account.

Think of this as your pre-flight checklist. By following these steps, you'll go into your first trade with confidence, knowing precisely what you're doing and why. The goal here is to make sure your first experience is a solid, educational one.

Step 1: Select a Quality Stock You Want to Own

This is, without a doubt, the most important rule of the game. Never sell a put on a company you wouldn't be genuinely happy to own for the long haul. This single principle is your ultimate safety net.

Look for stable, fundamentally sound companies with a proven track record. This isn't the time to dabble in highly volatile, speculative, or "meme" stocks. You want to be completely comfortable with either of the two outcomes: you keep the premium as pure profit, or you buy shares of a great company at a discount.

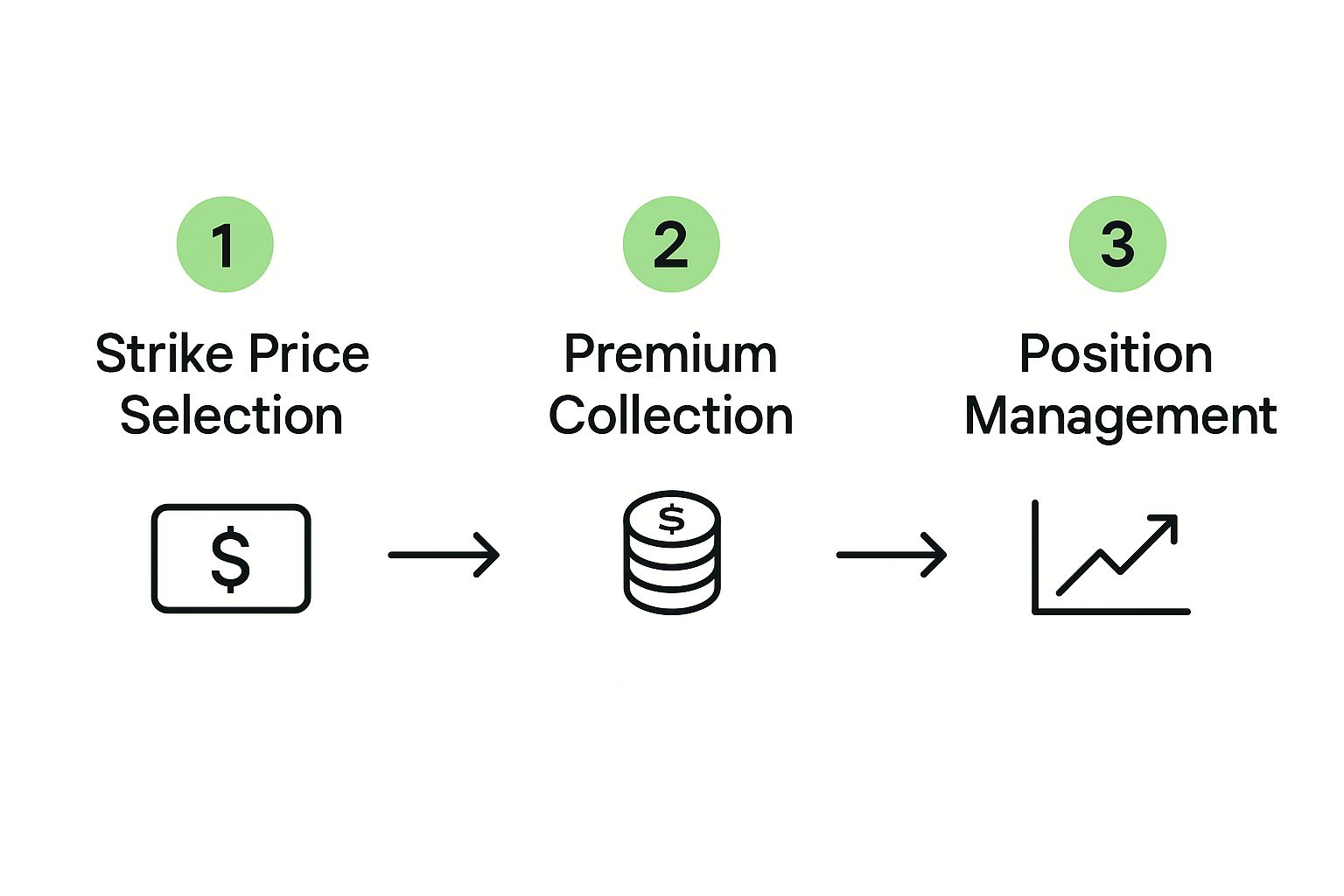

Step 2: Choose the Right Strike Price

The strike price is the specific price you’re agreeing to buy the stock for if it drops. Choosing it is a bit of a balancing act between how much income you want to generate and the price you’d feel great about paying for the stock.

- Higher Strike Price (Closer to the current stock price): This will net you a much fatter premium. The trade-off? There's a higher chance the option will finish "in-the-money" and you'll be assigned the shares.

- Lower Strike Price (Further from the current stock price): You'll collect a smaller premium, but the probability of being assigned the stock drops significantly. This is the more conservative play.

A solid approach is to pick an out-of-the-money (OTM) strike price that lines up with a technical support level on the stock's chart or a valuation you’ve already determined is attractive.

This visual shows how your decisions flow together. It all starts with the strike price, which directly impacts the premium you collect and dictates how you'll manage the position down the road.

Step 3: Pick a Suitable Expiration Date

The expiration date simply sets the clock on your obligation. How long are you willing to wait? Options with more time left on the clock always command higher premiums, mainly because there's more time for the stock price to make a big move.

For most traders, an expiration date between 30 and 45 days out hits the sweet spot. It offers a respectable premium without tying up your capital for an eternity. Shorter-term options, like weeklies, have faster time decay (which is good for sellers!), but they also require you to be much more hands-on.

Step 4: Calculate Your Key Metrics

Before you pull the trigger, you absolutely have to run the numbers. It’s just simple math, but it's crucial for understanding any sell put strategy.

- Maximum Profit: This is easy—it’s the premium you collect upfront. If you sell one contract for a $2.00 premium, your max profit is $200 (since one contract represents 100 shares, it's $2.00 x 100).

- Required Capital (Collateral): For a cash-secured put, the "secured" part means you have the cash ready to buy the shares. To find this number, just multiply Strike Price x 100. For a $50 strike, you'll need $5,000 of cash set aside in your account.

- Break-Even Price: This is your true cost basis if you end up buying the stock. Calculate it as Strike Price - Premium Received. With a $50 strike and that $2.00 premium, your real break-even cost is $48.00 per share.

Key Insight: As long as the stock stays above your break-even price by expiration, you won't have an unrealized loss on the position. That premium you collected acts as an immediate, upfront discount on your potential purchase.

Step 5: Execute the Trade

Alright, you've done your homework. You have your stock, strike price, and expiration date. It's time to head to your brokerage platform. The process is pretty standard across the board.

- First, pull up the options chain for your chosen stock.

- Make sure you’re looking at the "Put" side of the chain, not the calls.

- Select the expiration date you picked out earlier.

- Find your strike price in the list and click on the "Bid" price. This should bring up a "Sell to Open" order ticket.

- Enter the number of contracts you want to sell (just start with one!).

- Carefully review the order details—check the premium, the collateral required, and any commissions.

- If it all looks good, submit the trade.

The moment your order gets filled, that premium cash is deposited into your account, and your brokerage will set aside the required collateral. For a more detailed breakdown with specific examples, check out our in-depth guide on selling cash-secured puts.

Congratulations! You're now in the trade and will manage the position until it expires.

Seeing the Sell Put Strategy in Action

Theory is a great starting point, but the real lessons come from seeing how a strategy plays out in the wild. To make these concepts click, let's walk through three different scenarios that every put seller will likely face at some point.

Each of these examples follows a unique path, showcasing just how versatile the sell put strategy can be under different market conditions. We'll use real numbers to break down the mechanics, the money, and the mindset behind each trade.

Scenario 1: The Pure Income Play

Let's say you've had your eye on a solid blue-chip company, "Tech Innovators Inc." (TII), which is currently trading at $125 per share. You like the company's fundamentals but think the stock is a bit pricey right now. You’d feel much better about buying it if it dipped closer to $115.

Instead of just sitting on your hands and waiting, you decide to get paid for your patience.

- Your Action: You sell one cash-secured put contract on TII with a $115 strike price that expires in 30 days.

- Premium Collected: For taking on this obligation, you immediately get a premium of $2.50 per share. That’s $250 deposited right into your account ($2.50 x 100 shares).

- The Outcome: The next month is pretty quiet. TII's stock price meanders a bit and closes at $122 on expiration day.

So, what happens? Because the stock price finished well above your $115 strike price, the put option expires worthless. The buyer has zero incentive to "put" the shares to you at $115 when they could get $122 on the open market.

Your obligation simply vanishes. The $11,500 you set aside as collateral is freed up, and you get to keep the $250 premium, no strings attached. This is the dream scenario for pure income generation.

Scenario 2: The Strategic Acquisition

Let's rewind and play the tape again with TII. This time, however, the market has other ideas. You still firmly believe that $115 is a fantastic price to get into this quality company.

You put on the exact same trade: selling a $115 put for that sweet $250 premium.

- The Outcome: A week before expiration, some shaky news hits the tech sector, and TII's stock takes a hit. On expiration day, it closes just below your strike at $114 per share.

- Assignment: Since the stock price is now below $115, you get assigned. It's time to fulfill your end of the bargain.

Your brokerage automatically uses the $11,500 you had secured to buy 100 shares of TII. You now officially own the stock, having bought it right at your target price. But the story gets even better.

The premium you collected from the start acts as an instant rebate on your purchase. It turns a good entry price into a great one.

Think about it: your cost basis isn't really $115 per share. Once you account for the $250 premium you pocketed, your effective purchase price is actually $112.50 per share. ($11,500 cost - $250 premium = $11,250 / 100 shares). You just bought a great company for even less than you were hoping for.

Scenario 3: Navigating a Downturn

Alright, now for the scenario that really tests a trader's discipline. You sell the same $115 put on TII and collect your $250 premium. But this time, the market decides to throw a real tantrum.

- The Outcome: Some unexpectedly bad economic data sends the entire market into a tailspin. On expiration day, TII has been dragged down with it, closing at $105 per share.

- Assignment: You are assigned the shares at your agreed-upon strike price of $115.

You now own 100 shares of TII, but you paid $11,500 for a position that's currently worth only $10,500. This leaves you with an immediate unrealized, or "paper," loss of $1,000 ($115 purchase price - $105 market price = $10 x 100 shares).

It stings, but your actual situation isn't quite that bleak. Remember that $250 premium? Your break-even price was always $112.50, which means your real unrealized loss is $750 ($112.50 - $105 = $7.50 x 100 shares).

This is the core risk of selling puts: you can be forced to buy a stock as its price is falling. But here’s the key—because you chose a quality company you wanted to own anyway, this isn't a disaster. You can now hold the shares and wait for a recovery, or even start selling covered calls against them to generate new income and lower your cost basis even further.

Comparing Put Selling Scenarios

To see these outcomes side-by-side, let's break down the numbers in a simple table. It helps visualize how the same initial trade can lead to very different financial results depending on the stock's price at expiration.

| Metric | Scenario 1 (Ideal Income) | Scenario 2 (Strategic Acquisition) | Scenario 3 (Managing a Loss) |

|---|---|---|---|

| Stock Price at Expiration | $122.00 | $114.00 | $105.00 |

| Strike Price | $115.00 | $115.00 | $115.00 |

| Initial Premium Received | $250 | $250 | $250 |

| Assigned Shares? | No | Yes | Yes |

| Effective Purchase Price | N/A | $112.50 / share | $112.50 / share |

| Immediate Profit/Loss | +$250 (Profit) | -$850 (Unrealized Loss) | -$750 (Unrealized Loss) |

| Final Position | Keep the cash | Own 100 shares | Own 100 shares |

As you can see, the outcome isn't just about profit or loss. It's about whether you achieved your goal—be it income, stock ownership, or managing a position through turbulence. Each scenario highlights a different strength of the put-selling strategy.

How to Manage and Optimize Your Positions

Getting into a trade is easy. Getting out with a profit? That’s where the real skill comes in. Actively managing your position is what separates the consistently profitable traders from those who just get lucky once in a while.

Great position management isn’t about frantically reacting to every market hiccup. It's about knowing when and how to make calculated adjustments—whether that means defending a trade that’s gone a bit sideways or just setting it up for success from the very beginning.

Keep an Eye on Volatility and the Greeks

Implied volatility (IV) is the engine of an options trade. Simply put, higher IV means the market is expecting bigger price swings. For an option seller, that’s great news because it translates directly into fatter premiums. Selling puts when IV is high is a classic way to boost your potential income right from the start.

But IV is just part of the story. You also need to keep a close watch on the "Greeks"—a set of metrics that tell you how sensitive your option is to different market forces. For instance, Delta gives you a quick-and-dirty probability of the option expiring in-the-money. A put with a Delta of 0.20 has roughly a 20% chance of being assigned. To get a better handle on these crucial metrics, you can learn more about what the option Greeks are in our detailed guide.

Mastering the Art of Rolling a Position

So, what happens when a trade starts moving against you and the stock price is creeping dangerously close to your strike price? Don't panic. This is where one of the most powerful tools in your arsenal comes into play: rolling the position. This isn't about admitting defeat; it's a strategic move to buy yourself more time or get a better price.

Rolling is a two-part maneuver you execute at the same time:

- Buy to Close your current put option (this might be for a small loss).

- Sell to Open a new put option on the same stock, but with a later expiration date, a lower strike price, or both.

The goal here is to collect enough premium from the new option to more than cover the cost of closing the old one. By rolling, you can push the trade further out in time, giving the stock more room to recover, and you can often lower your risk by moving down to a safer strike.

Rolling a position is a proactive technique to manage risk. It allows you to collect more premium and adjust your break-even point, turning a potentially losing trade into a winning or break-even one.

Choosing Between Weekly and Monthly Options

The expiration cycle you choose has a huge impact on both your income potential and your risk. Weekly options offer a faster pace and more frequent income, while monthlies are a bit more relaxed.

- Weekly Options: These expire every week, which means you can collect premium and compound your returns much more frequently. Thanks to rapid time decay (theta), you can often generate higher annualized premiums this way.

- Monthly Options: These give your trade more breathing room and require less hands-on management. The upfront premiums are larger, but they tend to be lower on an annualized basis compared to weeklies.

The data backs this up. Research on put-writing indices has shown some pretty compelling results for shorter-term strategies. For example, the Weekly PutWrite index (WPUT) collected an average of 37.1% in annual gross premiums between 2006 and 2018. The monthly version? It brought in 22.1%. This suggests a weekly approach can not only generate more income but might even do so with lower risk exposure. You can dig into the full research paper to discover more on these findings.

Common Questions About Selling Puts

Even after you've got the basics down, a few questions always seem to pop up when you're starting out with selling puts. That's perfectly normal. Let's walk through some of the most common ones to help build that last bit of confidence you need to get started.

Think of this as the final checklist before you place your first trade. Getting these concepts straight is key to managing your risk and feeling comfortable with the strategy.

Cash-Secured vs. Naked Puts

One of the biggest points of confusion is the difference between a "cash-secured" put and a "naked" put. The distinction is absolutely critical for managing your risk.

A cash-secured put is exactly what it sounds like. You have the cash on hand to buy the stock if it gets assigned to you. If you sell one put contract with a $50 strike price, you need to have $5,000 ($50 strike x 100 shares) sitting in your brokerage account, ready to go. This is a defined-risk approach and the standard for most investors.

A "naked" or "unsecured" put is the wild west of options trading. It means you sell the put without having the cash to back it up. This is an incredibly high-risk move that can lead to massive, theoretically unlimited losses. It requires special approval from your broker and is not something most individual investors should ever consider. For our purposes, we're always talking about cash-secured puts.

Understanding Stock Assignment

So, what actually happens if the stock price drops and you get assigned?

If the stock closes below your strike price on the expiration date, you're "assigned." This just means you're fulfilling your end of the contract: you are now obligated to buy 100 shares of the stock (per contract) at the strike price you chose. The $5,000 you set aside for that $50 strike put? It's now used to buy those shares.

Congratulations, you're now a shareholder! From here, you have options. You can hold onto the stock for the long term, sell it right away (for a potential loss or gain), or even start selling covered calls against your new shares to generate more income.

Choosing the Right Stock

This might be the most important question of all: how do you pick the right stock?

The golden rule is simple but powerful: only sell puts on stocks you would be genuinely happy to own at the strike price.

Forget about chasing high premiums on volatile, speculative stocks. That’s a recipe for ending up with a portfolio full of companies you don't believe in, bought at a price that's still falling. Instead, focus on high-quality businesses you've already researched and would be comfortable holding for the long haul. This way, either outcome is a win—you either keep the premium for free, or you get to buy a great company at a discount.

Ready to turn guesswork into a data-driven process? Strike Price provides real-time probability metrics for every strike price, helping you balance safety and premium. Our smart alerts and tracking dashboard empower you to sell puts with confidence. Start making informed decisions today at https://strikeprice.app.