How Options Are Priced A Practical Guide for Investors

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

Out of Money Call Options A Guide to Consistent Income

Learn how to use out of money call options to generate consistent income. This guide covers key strategies, risk management, and real-world examples.

Greek Options Explained for Income Traders

Unlock your options trading potential. This guide on greek options explained shows you how to use Delta, Gamma, and Theta to generate consistent income.

How to Trade Stock Options for Steady Weekly Income

Learn how to trade stock options with a simple, data-driven approach. This guide covers covered calls, puts, and risk management for consistent income.

An option's price, known as the premium, is a mix of its real, immediate value and its potential future value. Think of it like a ticket to a big game. The price reflects not just where the teams stand today, but also the excitement and possibility of a future win.

This blend of "here-and-now" value and "what-if" potential is the secret sauce behind how every option is priced.

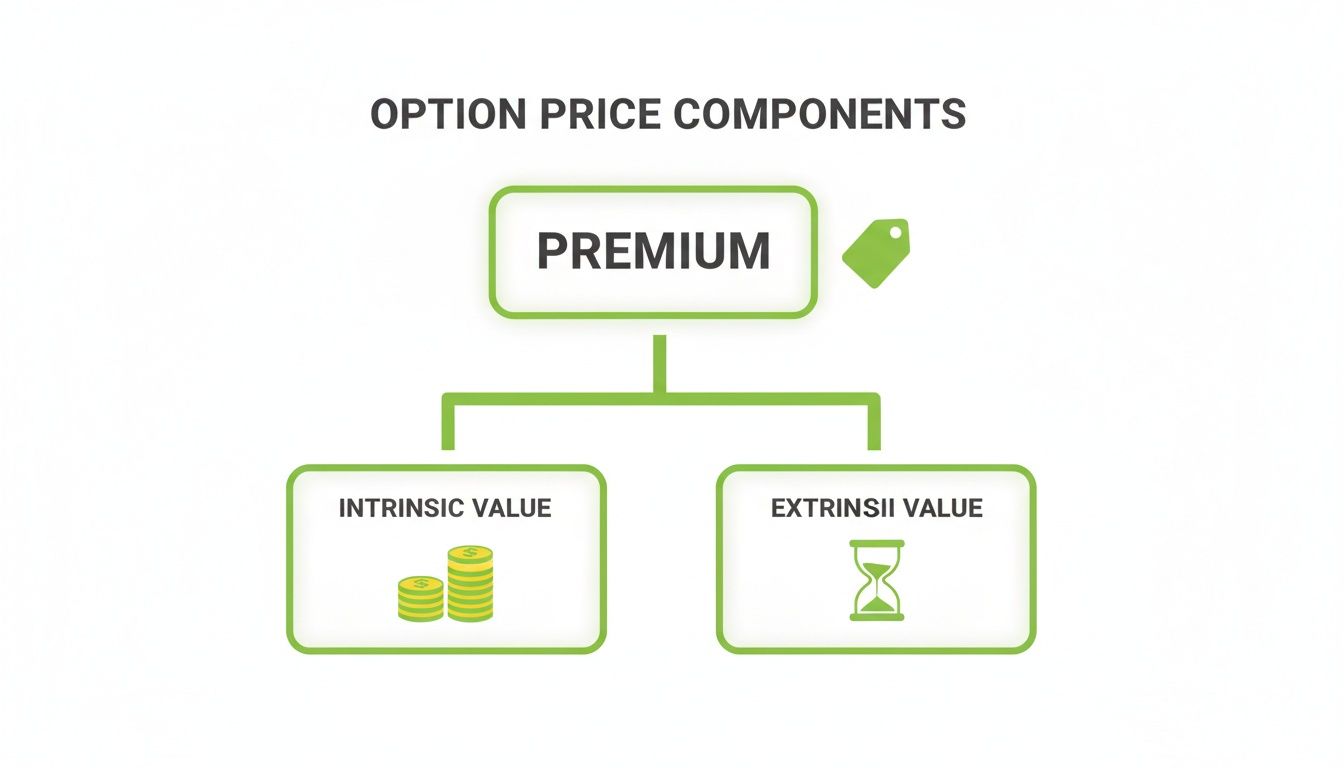

Deconstructing an Option’s Price Tag

To really get a handle on options pricing, you need to see the premium not as one number, but as two separate parts working together: Intrinsic Value and Extrinsic Value. Getting this concept down is the single most important first step for anyone serious about trading options.

Every single option premium you see boils down to one simple equation:

Premium = Intrinsic Value + Extrinsic Value

This isn't just some textbook theory. It's the practical logic every trader, market maker, and pricing model uses to figure out what an option is worth from one moment to the next. Let's pull back the curtain on each piece.

Intrinsic Value: The Here-and-Now Worth

Intrinsic value is what an option would be worth if you exercised it right this second. It's the straightforward, no-fluff part of the price. For a call option, it only exists if the stock is trading above your strike price. For a put, it’s the other way around—the stock has to be below the strike.

- Example: If a stock is trading at $105, a call option with a $100 strike price has exactly $5 of intrinsic value ($105 - $100). The option is "in-the-money."

An option can never have negative intrinsic value. If it's out-of-the-money, its intrinsic value is simply $0. It has no immediate value if exercised.

Extrinsic Value: The What-If Worth

This is where things get interesting. Extrinsic value, which you’ll often hear called "time value," is everything else. It’s the potential, the hope, the uncertainty—all rolled into one number. It's the premium you pay for the chance that the option could become profitable before it expires.

Think of it as the speculative fuel in the option's price. The more time an option has until its expiration date and the more wildly the stock is expected to swing (its volatility), the higher the extrinsic value will be. Why? Because there’s more time and more opportunity for the stock price to make a big move in your favor.

This "what-if" value is driven by a few key factors we'll dig into next:

- Time to Expiration: A longer runway gives the stock more chances to take off.

- Implied Volatility: The market's best guess on how much the stock will jump around.

- Interest Rates & Dividends: Smaller players, but they still have a seat at the table.

To put it all together, let’s look at a simple breakdown.

The Two Halves of an Option's Price

| Component | What It Represents | Key Analogy |

|---|---|---|

| Intrinsic Value | The option's immediate, tangible worth if exercised now. | The "down payment" on a house—it's real equity. |

| Extrinsic Value | The potential for the option to gain value over time. | The "market buzz"—hope, time, and uncertainty. |

Understanding these two halves—the concrete intrinsic value and the ever-changing extrinsic value—is the bedrock of making smarter, more confident decisions when you’re selling options for income. It’s how you move from guessing to making calculated trades.

The Five Core Drivers of Option Prices

An option's premium isn't some random number pulled out of thin air. It’s a carefully calculated price based on five key ingredients. Think of it like baking: the market combines several distinct factors to determine what an option is worth.

Getting a handle on these drivers is the secret to understanding why you get paid a certain premium to sell a contract.

The final price is always a mix of the option's real, tangible value (intrinsic value) and its potential future value (extrinsic value).

Let's break down each of the five ingredients that shape an option's final price.

1. Underlying Stock Price

This one is the most obvious. The price of the underlying stock has a direct, immediate impact on an option's value. As the stock moves, so does the option's intrinsic worth.

For a call option, its value goes up as the stock price climbs past the strike. For a put option, it becomes more valuable as the stock falls below the strike. This relationship is the bedrock of an option's price.

- Example: You sell a $100 strike call when the stock is at $102. That option has $2 of real, intrinsic value. If the stock suddenly shoots up to $105, the intrinsic value instantly jumps to $5.

2. Time to Expiration

For an option seller, time is a powerful ally. The more time an option has until it expires, the more chances the stock has to make a big move. That uncertainty makes the option more valuable.

I like to think of an option's time value as a melting ice cube. Every single day, a little piece of its value disappears forever. This process is called time decay, or Theta.

When you sell an option, you're essentially selling that melting ice cube to someone else. You profit as its value drips away, day by day. This is why selling shorter-term options, like weeklies, can be such a potent income strategy.

Key Insight: As an option seller, time is your best friend. Every day that passes without a big, unfavorable move in the stock price, a portion of the premium you collected turns into realized profit.

3. Implied Volatility

If time is your best friend, then implied volatility (IV) is the engine that powers your potential income. IV is simply the market's forecast of how much a stock’s price is expected to swing. People often call it the "fear gauge."

When there's a lot of uncertainty—maybe right before an earnings report or during a market panic—implied volatility goes through the roof. This inflates option premiums because the odds of a huge price swing are higher.

For a seller, high IV is an opportunity. It means you can collect a much bigger premium for taking on the same fundamental risk. A common goal is to sell options when IV is high and then profit as it drifts back to normal levels—a phenomenon known as a "volatility crush."

4. Interest Rates

Interest rates play a more subtle role, but they're still part of the equation, especially for longer-dated options. The risk-free interest rate affects the cost of carrying the underlying stock.

Here's the general rule of thumb:

- Higher interest rates tend to increase the price of call options.

- Higher interest rates tend to decrease the price of put options.

While the impact is often tiny for options expiring in a few weeks, it becomes a much more noticeable factor for contracts that are six months or a year out.

5. Dividends

Finally, dividends have a direct and predictable effect on option prices. When a company pays a dividend, its stock price is expected to drop by the dividend amount on the ex-dividend date.

Pricing models account for this expected drop in a pretty logical way:

- It decreases the value of call options because the stock is expected to fall.

- It increases the value of put options for the exact same reason.

You don't have to calculate this yourself; it's automatically baked into the premium you see on your screen.

These five drivers are the foundation. To really take control, your next step is to understand how an option's price reacts to changes in these factors. That’s where the Option Greeks come in—they measure the sensitivity of your option's price to each of these drivers.

Implied Volatility: The Real Engine of Premium

If an option's price is a recipe, then implied volatility (IV) is the most potent spice. While the stock price sets a baseline and time provides a predictable decay, IV is the wild card that truly determines how expensive or cheap an option is.

For income-focused sellers, mastering implied volatility isn't just a good idea—it's the core of the business.

Think of implied volatility as the market's "fear and greed gauge." It doesn't look backward; instead, it represents the collective expectation of how much a stock's price will swing in the future.

Why IV Is an Option Seller's Best Friend

Imagine you're selling car insurance. You'd charge a much higher premium to insure a race car driver than you would for a librarian who drives once a week. The risk is higher, so the price of protection is higher. Options work the exact same way.

When the market expects big news—like an earnings report, a product launch, or an FDA decision—uncertainty spikes. This increased expectation of price movement inflates option premiums across the board.

- High IV: The market anticipates big price swings, so options are more expensive. This is a seller's market, as you can collect more premium for the risk you take.

- Low IV: The market expects calm seas, so options are cheaper. This is generally a better environment for option buyers.

As a seller, your goal is simple: sell insurance when the perceived risk (and thus, the price) is high. You collect a fat premium upfront, hoping the expected chaos never materializes.

IV isn't just a component of an option's price; it's the heartbeat, often dictating 70-80% of an at-the-money option's extrinsic value. It’s the market’s forward-looking forecast, a stark contrast to historical volatility, which just measures past price wiggles.

The Power of Volatility Crush

One of the most predictable patterns in options trading is the volatility crush. This happens when IV plummets after a known event has passed. Think about the tension before a major company's earnings announcement—IV will be sky-high as traders brace for a big move.

Once the earnings are released, all that uncertainty vanishes in an instant. Regardless of whether the stock goes up or down, the expectation of a big swing is gone. As a result, implied volatility collapses, and option premiums get crushed.

For an options seller, this is a golden opportunity. By selling an option when IV is inflated before the event, you can often profit from this rapid decay in premium, even if the stock moves slightly against you.

Is Volatility High or Low Right Now?

Saying IV is "high" is meaningless without context. An IV of 50% might be extremely high for a stable utility stock like Consolidated Edison (ED) but unusually low for a volatile tech name like Palantir (PLTR). This is where relative metrics become crucial.

Two common tools help traders gauge this:

- IV Rank (IVR): This metric tells you where the current IV level stands in relation to its own highs and lows over the past year. An IVR of 95% means the current IV is in the top 5% of its 52-week range, indicating it's expensive relative to its own history.

- IV Percentile (IVP): This shows you what percentage of days in the last year the IV was lower than it is today. An IVP of 80% means that for 80% of the past year, volatility was lower than it is right now.

For options sellers, a high IV Rank or Percentile (typically above 50) signals a potentially attractive time to sell premium. It’s like a flashing sign that says, "Insurance is expensive right now!"

How IV Impacts Pricing in The Real World

Volatility is the direct engine of premium pricing. For instance, data from the 2008 financial crisis showed the VIX—the market's main IV gauge—rocketing from 20% to a staggering 89.53% after the Lehman Brothers collapse, causing some option prices to surge over 400% overnight.

In calmer times, like 2017, the S&P 500's IV stayed low around 9-12%, making weekly covered call premiums tiny. Fast forward to the March 2020 crash, IV hit 80%, and suddenly those same calls were yielding massive premiums. You can find more insights about historical volatility data on Optionistics.

This dynamic highlights why understanding IV is not just theoretical; it's the key to knowing how options are priced in real-time. By focusing on selling premium when IV is historically high, you put the statistical odds firmly in your favor, turning market fear into a reliable source of income. This sensitivity of an option's price to changes in IV is measured by a specific option Greek; check out our guide on what Vega is and how it works in options trading.

How Pricing Models Work Without the Math

So far, we've broken down an option's price into its core drivers—stock price, time, and volatility. But how do all those ingredients get mixed together to spit out one precise number? That’s where options pricing models come in.

Don't let the name intimidate you. Think of a pricing model less like a terrifying math equation and more like a sophisticated recipe. It takes the five key inputs we've covered, follows a specific formula, and gives us a theoretical "fair price" for any given option.

The most famous of these recipes is the Black-Scholes model.

The Black-Scholes Model: A Pricing Revolution

Believe it or not, before the 1970s, pricing options was mostly guesswork. There was no standard, widely accepted way to figure out what an option should be worth. That all changed in 1973.

Just as the options market was taking off with the launch of the Chicago Board Options Exchange (CBOE), Fischer Black, Myron Scholes, and Robert Merton rolled out their groundbreaking model. It was revolutionary because it treated an option's price as a direct function of five inputs: the stock price, strike price, time to expiration, risk-free interest rates, and volatility.

The impact was immediate and massive. By 1980, CBOE options volume soared to over 10 million contracts a year. Today, variations of this model are the engine behind the pricing of over 80% of listed options worldwide. Its influence is hard to overstate. If you're curious about the history, this research paper from Syracuse University is a great read.

For the first time, the model gave the entire market a common language for pricing. Traders everywhere could finally agree on a baseline value, which made the market more liquid and efficient for everyone.

At its core, the Black-Scholes model is built on a powerful idea: you can perfectly mimic an option's payoff by continuously buying and selling the underlying stock. The model simply calculates the cost of creating that perfect hedge, and that cost becomes the option's theoretical price.

Where Models Meet Reality: The Volatility Smile

While the Black-Scholes model is the industry standard, it has one famous flaw: it assumes that implied volatility is the same across all strike prices for a given expiration date. In a perfect world, if you graphed this, you'd see a flat, straight line.

But the real world isn't perfect. When you look at actual market prices, you see something else entirely—a curve often called a "volatility smile" or, more commonly, a "smirk."

This pattern reveals a fascinating quirk of market psychology. Traders are willing to pay a much higher premium for out-of-the-money put options than the model says they should. Why? They're buying "crash insurance." The higher IV on those puts reflects a collective fear that a sudden, sharp market drop is more likely than a sudden, sharp rally.

- What the model assumes: Volatility is constant for all strikes.

- What the market actually does: Prices in much higher volatility for downside protection (puts far from the current price), creating that classic "smirk" shape on a graph.

This is a perfect example of how pricing models and reality interact. The models give us an essential baseline, but the final price is always set by human behavior—fear, greed, and good old-fashioned supply and demand. Our detailed guide on the valuation of options digs deeper into these market dynamics.

For an options seller, this is gold. The volatility smile literally shows you where the market is paying the most for uncertainty. By understanding this, you can position your trades to collect the highest premium for the risks you’re actually comfortable taking.

Using Price to Understand Probabilities

An option's price isn't just a number; it's a story about probability. Once you learn how to read it, you can instantly see what the market expects and start making smarter, more calculated decisions. This is where all the theoretical drivers of price—volatility, time, the stock's movement—meet the practical reality of placing a trade.

This connection between price and probability is powered by the "Greeks." They might sound like something out of a finance textbook, but they’re actually incredibly practical. Think of them as the dashboard gauges for your option position, telling you exactly how its price will react when the market changes.

While there are several Greeks, one stands out for its immediate, practical use in understanding odds: Delta.

Delta as a Probability Shortcut

For anyone selling options for income, Delta is your most valuable guide. It tells you a couple of key things, but its most important job is serving as a quick-and-dirty probability estimate.

Delta gives you a rough approximation of the probability that an option will expire in-the-money (ITM).

This is a complete game-changer. Suddenly, you don't have to guess anymore. You can pull up an option chain and immediately see the market's baked-in odds for every single strike price.

- An option with a 0.30 Delta has roughly a 30% chance of finishing in-the-money.

- An option with a 0.15 Delta has roughly a 15% chance of finishing in-the-money.

This one insight transforms how you choose your trades. Instead of picking a strike price based on a gut feeling, you can align it directly with your personal risk tolerance. A conservative seller might only feel comfortable selling options with a Delta of 0.10 (just a 10% chance of assignment), while someone more aggressive might aim for a 0.30 Delta to collect a bigger premium.

Balancing Premium and Probability

This brings us to the fundamental trade-off every options seller faces. The higher the Delta—and therefore, the higher the probability of the option finishing in-the-money—the more premium you’ll collect. The market is literally paying you more to take on more risk.

Your job is to find the sweet spot that matches your goals.

- Low Delta (e.g., 0.10 - 0.20): You'll collect a smaller premium, but your probability of the option expiring worthless is much higher. This is the classic high-probability, lower-return approach.

- Higher Delta (e.g., 0.30 - 0.40): You'll pocket a much larger premium upfront. But the odds of your shares getting called away (for a covered call) are significantly greater. This is a lower-probability, higher-return strategy.

To really get a handle on this, it's essential to calculate your risk-reward ratio for any trade you're considering. It puts a hard number on the potential profit versus the potential loss, taking the guesswork out of the equation.

Ultimately, using Delta empowers you to trade with intention. It allows you to define your desired outcome—whether that’s maximizing income or maximizing safety—and then select the exact strike prices that give you the best shot at achieving it. Our guide on the probability of profit in options dives even deeper into this crucial concept.

Options Pricing FAQs

Even after you get the hang of the basics, a few questions about options pricing tend to pop up again and again. Let’s tackle some of the most common ones to clear up any confusion and help you trade with more confidence.

Think of this as your quick-reference guide.

What's the Single Most Important Factor for an Option Seller?

For anyone focused on income, the answer is hands-down implied volatility (IV). Yes, the stock price and time left are crucial, but IV is the engine that really pumps up the premium you collect.

Selling options is a lot like selling insurance. You want to sell that policy when the perceived risk is highest because that’s when people are willing to pay top dollar. High IV is the market’s way of saying it expects big price swings, which makes option premiums rich—creating the perfect setup for sellers.

Why Do Two Options on the Same Stock, at the Same Strike, Have Different Prices?

This almost always boils down to one simple thing: their expiration dates. An option with more time on the clock has more chances for the underlying stock to make a big move.

It’s like buying more lottery tickets. An option that expires in 90 days holds way more "what-if" potential than one expiring in just 10 days. That extra time translates directly into higher extrinsic value, making the longer-dated option more expensive. As a seller, you're getting paid more to take on risk over a longer stretch.

Key Takeaway: Every option is a decaying asset. The further out its expiration, the more time value is baked into its price. This value melts away a little each day—a process called time decay—which is exactly how option sellers make their money.

Historical vs. Implied Volatility—What's the Difference?

Getting this right is fundamental. Both measure volatility, but they’re looking in completely opposite directions.

- Historical Volatility (HV) is purely backward-looking. It’s a fact. It tells you how much a stock’s price actually bounced around in the past (say, over the last 30 days).

- Implied Volatility (IV) is forward-looking. It’s the market’s best guess of how much the stock will move in the future. This number is pulled directly from current option prices and is packed with trader sentiment, fear, and greed.

For any options trader, IV is what really matters. Premiums aren't priced on what a stock did, but on what the market thinks it’s about to do.

How Does a Dividend Affect Option Prices?

A dividend payment has a direct and predictable impact on an option's premium because everyone knows it will cause the stock's price to drop on the ex-dividend date. Pricing models are smart enough to account for this ahead of time.

- For Call Options: That expected price drop makes calls a little less valuable. Their prices will be a bit lower than they would be otherwise.

- For Put Options: The opposite is true here. An expected dip in the stock's price makes puts more valuable, so their prices will be slightly higher to reflect that.

This adjustment just ensures the option's price is a fair reflection of the stock's anticipated move.

Ready to stop guessing and start using data to find the best covered call and secured put opportunities? Strike Price provides real-time probability metrics for every strike, helping you balance income and risk with confidence. See how thousands of traders are earning consistent income by making smarter, data-driven decisions. Explore our platform and start your journey at https://strikeprice.app.