A Practical Guide to Selling Covered Calls for Income

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

Selling covered calls for income is a pretty straightforward concept: you're essentially renting out your shares of a stock you already own. In exchange, you get paid an upfront fee (the premium). It's a popular strategy for a reason—it’s a reliable way to generate a steady stream of cash flow from your portfolio.

The Mechanics of Generating Income with Covered Calls

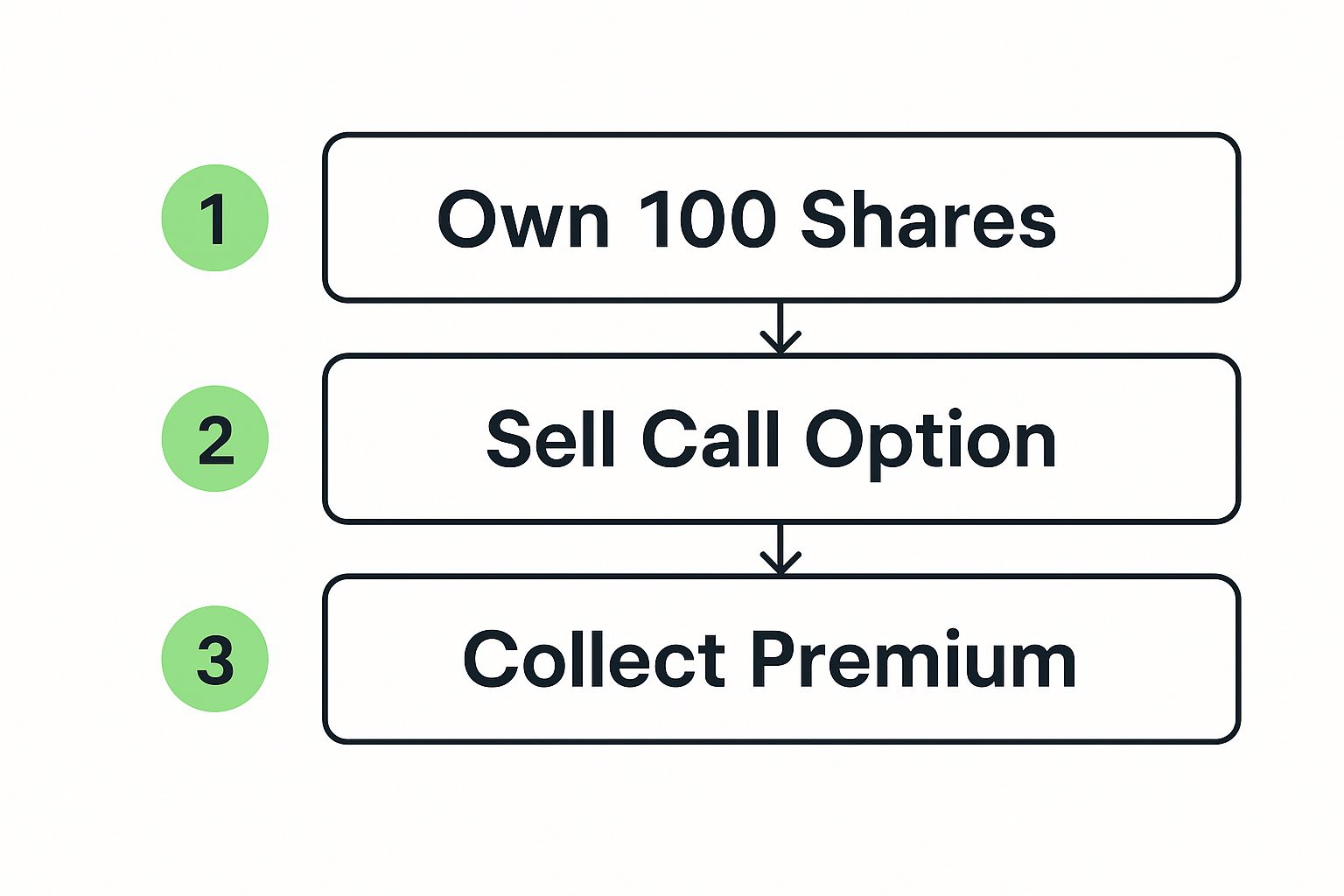

At its core, selling a covered call is a simple trade. You own at least 100 shares of a stock, and you agree to sell those shares at a specific price (the strike price) by a certain expiration date. For making that promise, you collect a cash premium right away.

That premium is yours to keep, no matter what happens next. It's an immediate return on your holdings, and it can be a great way to supplement dividend income. The best part? You can do this over and over again, month after month, on the same block of shares. This turns your stocks into an income-producing asset.

The Three Core Components

To really get the hang of it, you need to understand the three pieces that make up every covered call trade. Nailing these down is key to making smart decisions.

- The Underlying Stock: This is the foundation. You have to own at least 100 shares for every single call contract you sell. This is what makes the call "covered"—your shares are the collateral, guaranteeing you can deliver if the buyer exercises their option.

- The Premium: This is the cash you get paid upfront for selling the call. It's your income from the trade. The amount you receive depends on things like the stock's volatility, how much time is left until expiration, and how close the strike price is to the current stock price.

- The Obligation: When you sell a call, you’re accepting an obligation. If the stock's price shoots up past your strike price by expiration, you have to sell your 100 shares at that agreed-upon price. This is true even if the stock is trading much higher on the open market.

That's the fundamental trade-off: you get immediate income, but you cap your potential upside.

Key Takeaway: The goal here isn't to hit a home run on a stock that skyrockets. It's about systematically "renting" your shares to collect regular premiums, which lowers your cost basis and provides a consistent cash flow.

Before you jump in, it helps to have a solid grasp of the language. Here's a quick reference for the most important terms you'll encounter.

Key Covered Call Terminology Explained

| Term | What It Means for You | Practical Example |

|---|---|---|

| Underlying Asset | The stock or ETF you own (at least 100 shares of). | You own 100 shares of Apple (AAPL). |

| Call Option | The contract you sell, giving someone the right to buy your shares. | You sell 1 AAPL call contract. |

| Strike Price | The price at which you agree to sell your shares if assigned. | You choose a strike price of $180 for your AAPL call. |

| Expiration Date | The date the option contract expires. | Your AAPL call expires on the third Friday of next month. |

| Premium | The cash you receive upfront for selling the call option. | You receive $2.50 per share, or $250, for selling the contract. |

| Assignment | The process where the option buyer exercises their right to buy your shares. | AAPL stock rises to $185, and you are assigned to sell your 100 shares at $180. |

Having these terms down will make navigating your brokerage platform and setting up trades feel much more natural.

A Look at Historical Performance and Risk

The conservative nature of this strategy isn't just theory; it's backed by data. While covered calls might not always keep pace with holding stocks during a raging bull market, they historically offer some nice downside protection when things get choppy. For instance, one study looking at returns from 1986 to 1989 found that during the 1987 crash, covered call strategies lost a lot less than the stocks themselves and were far less volatile.

This really highlights the dual benefit: you generate income while taking some of the edge off the risk of just holding stocks. The premium you collect acts as a small cushion against falling prices. For a deeper look at how this all fits together, check out our complete guide on building a covered call income strategy.

Of course, when you start generating income, you also need to think about taxes. It's smart to look into strategies to minimize your capital gains tax liability to make sure you're keeping as much of your hard-earned premium as possible.

How to Select the Right Stocks for Covered Calls

The single most important decision you'll make in any covered call trade happens before you even look at an options chain. It's choosing the right stock. Get this part right, and everything else gets easier. Get it wrong, and you're just setting yourself up for a headache.

Think of it this way: you’re essentially agreeing to a long-term relationship with this stock. If the call expires worthless, you're still holding the shares. You have to be okay with that. If you wouldn't want to own the stock on its own merits, you have no business selling calls on it. That simple rule will save you a world of pain.

The Ideal Stock Profile

So, what makes a stock a good candidate for covered calls? You're not looking for a high-flying rocket ship that could double or crash overnight. You're looking for a dependable workhorse.

The best stocks for this strategy usually tick a few key boxes:

- Stable Price Action: The ideal stock moves in a predictable range or drifts gently upward. Wild volatility might offer juicy premiums, but it also means the stock could plummet, leaving you with a paper loss far bigger than the premium you collected.

- Plenty of Liquidity: Stick to stocks with high daily trading volume. This ensures you can get in and out of both the stock and its options without a fuss. High liquidity also means tighter bid-ask spreads, which saves you money on every trade.

- Dividend Payments: While not a dealbreaker, dividend stocks are fantastic candidates. These are often mature, financially healthy companies. The dividend gives you an extra stream of income on top of the call premium, boosting your total return.

A blue-chip name like Coca-Cola (KO) or Johnson & Johnson (JNJ) is often a much better fit than a speculative tech company. The movements are more measured, and you get that reliable dividend check.

What to Actively Avoid

Knowing what to avoid is just as crucial. Certain red flags should make you think twice before selling a call. The biggest one? A major catalyst on the horizon that could throw the stock's price into chaos.

The most common culprit here is an upcoming earnings report. The days before and after an earnings release are a minefield of volatility. A great report could send the stock soaring way past your strike, meaning you miss out on a huge rally. A bad one could cause it to crater, leaving you with a big loss that your premium can't hope to cover.

Pro Tip: Always, and I mean always, check the company’s investor relations calendar before you sell a call. If an earnings report is scheduled before your option expires, it's usually smarter to just sit on the sidelines or find another stock. That extra bit of premium isn't worth the gamble.

Putting It All Together

Your selection process needs to be methodical, not emotional. Start by building a watchlist of companies you actually believe in and wouldn't mind owning for the long haul. Then, pull up their charts. Look for that stable, predictable price action. You can even use modern AI-powered investment analysis tools to help you screen for these characteristics.

Once you have a solid candidate, check its options chain for good volume and tight spreads. Lastly, do a quick news check to make sure there are no bombshells like product launches or legal troubles on the horizon.

Nailing your stock selection is the first half of the battle. The next critical piece is figuring out how to choose an option strike price. This disciplined, step-by-step approach is what separates consistent income from pure speculation.

Choosing Your Strike Price and Expiration Date

Okay, you've picked a solid stock to work with. Now comes the real craft: selecting the contract. This is where your covered call strategy truly comes to life, because your choice of strike price and expiration date will define your potential income and your level of risk.

Nail this part, and you're on your way to a steady stream of premiums. Get it wrong, and you'll likely end up frustrated. Your brokerage platform's options chain is where you'll find all the available strikes and expirations. It looks like a wall of numbers at first, but it's your key to making smart trades.

The Art of Selecting a Strike Price

The strike price is the absolute cornerstone of your trade. It’s the price you agree to sell your 100 shares for if the option gets exercised. Choosing a strike is all about a trade-off: the premium you get versus the probability of your shares being sold.

There are three main ways to play it, each with its own flavor of risk and reward.

Out-of-the-Money (OTM): This is when you pick a strike price that is higher than where the stock is currently trading. An OTM call is the more conservative route. You'll pocket a smaller premium, but the stock has more room to run up before your shares are at risk of being called away. This is perfect if your main goal is to hold onto your shares while still generating some income.

At-the-Money (ATM): Here, the strike price is right around the current market price. ATM calls offer some of the fattest premiums because there's roughly a 50/50 shot the stock will end up above the strike. It maximizes your immediate income but also comes with a real risk of assignment.

In-the-Money (ITM): Picking a strike below the current stock price means the option is already in-the-money. You'll collect a very juicy premium, but there's a very high probability your shares will be sold. This is a move you make when you're ready to sell the stock anyway and want to squeeze some extra profit out of the exit.

Let's make this real. Say you own 100 shares of Microsoft (MSFT), trading at $425. Selling a call with a $440 strike (OTM) might only bring in a small premium, but it gives MSFT a $15 cushion before your shares are on the line. On the flip side, selling a $425 strike (ATM) would land you a much bigger premium, but you're at immediate risk of assignment if the stock just inches up.

This simple cycle—owning shares, selling a call, and collecting cash—is the engine that drives the whole strategy.

Strike Price Strategy Comparison

Deciding between these strategies can be tough, so here’s a quick breakdown to help you match a strike to your personal goals and risk tolerance.

| Strategy | Primary Goal | Premium Level | Best For |

|---|---|---|---|

| Out-of-the-Money (OTM) | Keep your shares, generate modest income | Lower | Investors who are bullish on the stock long-term |

| At-the-Money (ATM) | Maximize immediate premium income | Higher | Neutral outlooks where you don't expect a big move |

| In-the-Money (ITM) | Maximize profit on an exit | Highest | When you're ready to sell the stock anyway |

Ultimately, the best strategy is the one that lets you sleep at night. If losing your shares would sting, stick with OTM. If you're all about that weekly income, ATM might be your game.

Finding the Expiration Date Sweet Spot

Just as critical as the strike price is the expiration date. It sets how long you're locked into the trade and has a huge impact on your premium. This is all thanks to something called time decay, or theta.

Think of options as melting ice cubes. They lose a little bit of value every single day, which is fantastic news for you as the seller.

For many traders, the sweet spot for selling options is 30 to 45 days out. This timeframe hits a great balance. You get a respectable premium upfront, and you also get to take advantage of accelerated time decay as the expiration date gets closer.

Shorter-dated options, like weeklys, decay super fast but offer smaller premiums and demand you be more hands-on. Longer-dated options give you bigger premiums but tie up your shares for months, leaving you exposed to more market curveballs.

Your decision here really needs to match your investment style and how much time you want to spend managing your trades. Find a rhythm that works for you. For a much deeper dive into timing your trades, our article on when to sell covered calls is a great next read.

When you pair the right strike with the right expiration, you're not just holding a stock—you're running a small income business.

How to Manage Your Covered Call Positions

Selling the call is just the first step. The real art of generating steady income from this strategy lies in what you do after the trade is placed. This is where you separate disciplined, process-driven investing from reactive guesswork.

https://www.youtube.com/embed/jfaABy0E6r4

Once your covered call is live, the trade can really only go one of three ways. Think of it like steering a ship you've just launched—you know the destination, but you have to navigate the market's waves to get there smoothly.

Let's walk through the playbook for each potential outcome.

Scenario 1: The Stock Price Stays Below the Strike

This is the best-case scenario for a pure income strategy. If the stock hangs out below your strike price as expiration day rolls around, the option contract you sold simply expires worthless.

That's a win.

You keep 100% of the premium you collected upfront, and you also keep your 100 shares of stock. The income engine just completed a full cycle. Now you’re free to turn around and sell a brand new call option for the next expiration period, kickstarting another round of income on those same shares.

Scenario 2: The Stock Price Rises Above the Strike

This is what’s known as assignment. It might feel like a mixed bag at first, but it's a completely normal—and often profitable—part of the process. If the stock's price is above your strike at expiration, the person who bought your call will almost certainly exercise their right to buy your shares.

When that happens, you are obligated to sell your 100 shares at that agreed-upon strike price. You still keep the entire premium, plus you've profited from the stock's appreciation all the way up to the strike.

The trade-off? You miss out on any gains the stock makes beyond that strike. This is the fundamental compromise you make when selling covered calls.

Mindset is Key: You absolutely cannot look at assignment as a "loss." You went into the trade knowing your maximum profit, and you hit it. That’s a successful trade, period. Fighting the urge to get frustrated over "missed" gains is what will keep you disciplined enough to stick with your income plan.

Proactive Management: Rolling Your Position

So, what if the stock is creeping up toward your strike and you'd rather not sell your shares? Or maybe the stock has dropped, and you want to collect a bit more cash to make up for it? This is where an incredibly useful technique called "rolling" comes into play.

Rolling a position is just two trades executed at the same time:

- Closing the current position: You buy back the exact same call option you originally sold.

- Opening a new position: You immediately sell a new call option on the same stock, but for a later expiration date and, usually, a different strike price.

This is your go-to move for actively managing your positions.

For example, if the stock is getting too close to your strike for comfort, you can roll up and out. This means you close your current call and sell a new one with a higher strike price and a later expiration date. This maneuver often brings in another credit (more income!) while giving the stock more room to climb before you risk assignment.

On the flip side, if the stock has fallen since you sold the call, you can roll down and out to a lower strike price. This lets you collect a much more substantial premium for the next cycle, putting your capital to work more efficiently.

Your goal is to always be in the driver's seat. Selling that initial call just sets the stage; the real performance is in how you manage the outcomes. This continuous cycle of selling, managing, and repeating is what transforms a static stock holding into a dynamic income-generating asset.

Common Covered Call Mistakes to Avoid

Learning to generate consistent income from covered calls is as much about dodging common errors as it is about making brilliant moves. The path is littered with potential missteps that can quickly sour a solid strategy. Knowing these pitfalls ahead of time is your best defense.

The most common trap? Chasing those sky-high premiums. When you see an option offering a massive return, it’s almost always tied to a highly volatile, unpredictable stock. Selling a call on a stock like this feels fantastic when you pocket the premium, but that feeling vanishes if the share price tanks, leaving you with a paper loss that dwarfs your income.

Getting Emotionally Attached to Your Stock

A classic blunder is falling in love with a stock and refusing to let it go, even when the trade says you should. Imagine you own 100 shares of your favorite tech company and sell a call. The stock then takes off, soaring past your strike price.

Instead of booking the win you planned for, you feel the sting of regret over those "missed" gains. This emotional reaction leads to bad decisions, like buying back the call for a big loss just to keep the shares. A successful covered call strategy demands treating assignment as a win—you hit your max profit goal for that trade.

To protect your capital and keep emotions out of the driver's seat, you need to implement effective risk management strategies. Discipline is what separates the pros from the amateurs.

Ignoring the Impact of Assignment and Taxes

Many new sellers get so focused on the premium income they forget what happens next. When your shares get called away, it's a taxable event. The premium you received is added to your sale price, which determines your final capital gain or loss.

Forgetting this can lead to a nasty surprise come tax season. Always factor in the potential tax hit before you enter a trade, especially if assignment would trigger a large short-term capital gain.

Key Insight: A successful covered call seller is a disciplined operator, not an emotional speculator. The goal is to consistently execute a plan, accepting all logical outcomes—including assignment—as part of a profitable, long-term income strategy.

The Danger of Aggressive Yield Chasing

Chasing the highest possible yield is a recipe for long-term disappointment. It's tempting to sell calls that promise huge monthly returns, but this often means you're taking on way too much risk.

Research backs this up. Studies looking at 'high-yield' call selling strategies targeting monthly yields up to 1.5% between 1999 and 2023 actually saw annualized losses of around -3.1%. This shows that bigger premiums often come with bigger capital losses, highlighting the delicate balance between income and risk.

A more sustainable path is to aim for reasonable, steady returns on stable stocks. By sidestepping these common mistakes, you build the foundation for a durable income stream, turning what could be a gamble into a reliable financial tool.

Frequently Asked Questions About Covered Calls

Even with a solid game plan, you're bound to have questions. It’s a normal part of learning any new strategy, and covered calls are no different. A few questions pop up constantly, and getting them answered is key to building the confidence you need to manage your trades well.

My goal here is to tackle the big ones head-on. Let's clear up any lingering uncertainty so you can move forward with your income strategy.

What Are the Tax Implications of Selling Covered Calls?

The premium you collect from selling a call has tax implications, and how it’s treated depends on what happens with the trade.

If the option expires worthless, the IRS generally views that premium as a short-term capital gain in the year it expires. Simple enough.

But if your shares get assigned, the premium you received is added to your total sale price for the stock. This new total is then used to calculate your capital gain or loss on the shares themselves. Just be aware that selling certain calls can sometimes mess with the holding period for long-term capital gains, so it’s a small detail worth paying attention to.

Can I Lose Money Selling Covered Calls?

Yes, you absolutely can, but it’s crucial to understand where the real risk is. The risk isn't from selling the call option itself; it's from owning the underlying stock.

If the stock's price takes a nosedive, the value of your shares will drop. That loss can easily be much larger than the premium you pocketed.

The premium you get acts as a small but valuable buffer. For example, if you own a stock at $50 a share and collect a $2 premium, your break-even price drops to $48. The strategy doesn't make you immune to losses, but it does reduce them by the amount of income you bring in.

What Happens If My Stock Pays a Dividend?

As the owner of the stock, you get to keep any dividends paid out, as long as you own the shares through the ex-dividend date. It’s a fantastic way to stack another layer of income on top of your call premiums.

There’s a catch, though. A savvy call buyer might exercise their option early—specifically right before the ex-dividend date—to snag that dividend for themselves. This is most common when your call is deep in-the-money, meaning the stock price has climbed far above your strike price. If your shares get called away before that date, you'll miss out on the dividend payment.

Ready to stop guessing and start making data-driven decisions? Strike Price provides real-time probability metrics for every trade, helping you balance safety and premium income. Turn your guesswork into a strategic income plan today.